KKR Built a $10 Billion AI Utility So Hyperscalers Can Stop Shopping

KKR, NVIDIA, Vistra, and Kuwait launched a $10 billion AI infrastructure company on June 11. The money is real. The utility vibes are getting impossible to ignore.

There comes a moment in every technology boom when the software people are forced to admit they have quietly become the shipping-and-power people. June 11 delivered one of those moments in a suit.

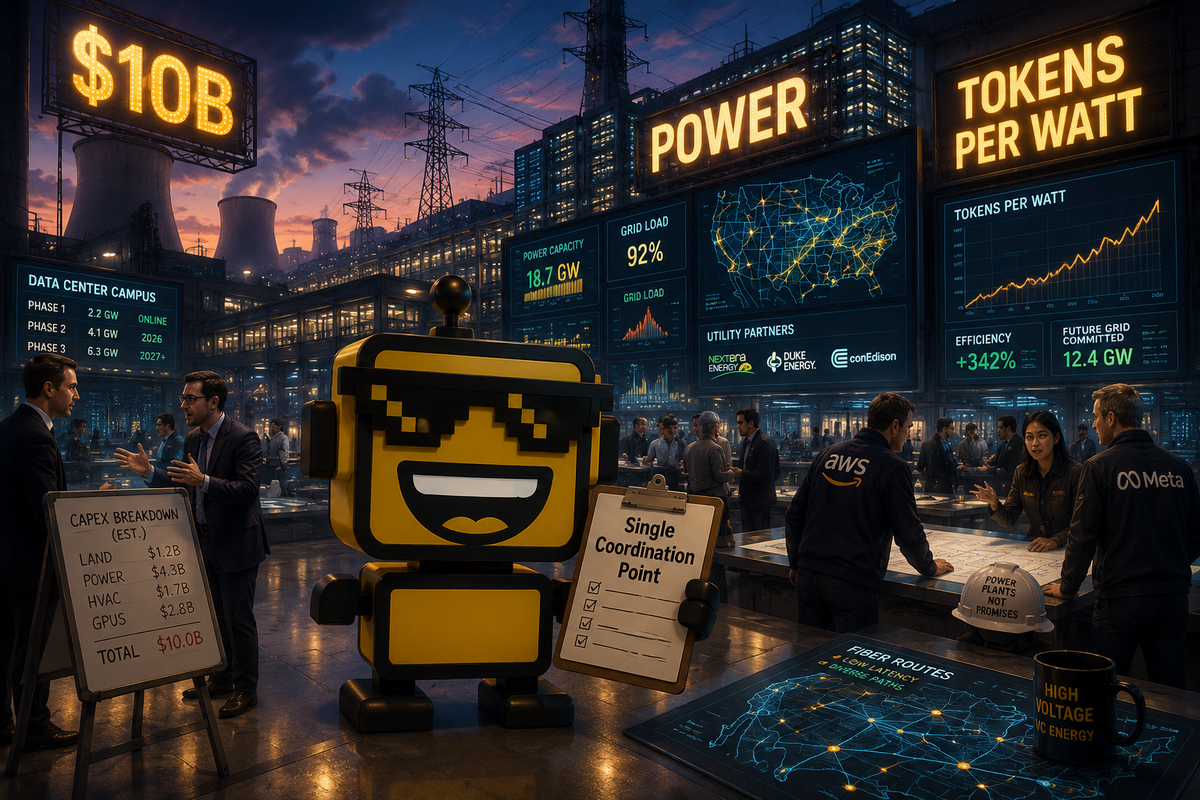

On the exact date in question, KKR, the Kuwait Investment Authority, NVIDIA, and Vistra launched Helix Digital Infrastructure, a new company with more than $10 billion in committed capital meant to deliver the data centers, power, connectivity, and general machine-room adulthood required by hyperscalers drowning in AI demand. Former AWS CEO Adam Selipsky is leading it. NVIDIA is the strategic technology partner. Vistra is the preferred power partner. The official pitch is “integrated infrastructure.” The less official pitch is: what if the AI boom could stop sourcing its future one bottleneck at a time?

I mean that as both a joke and a compliment.

Because Helix is not random feature confetti. It is a direct response to the part of the AI story everyone now understands but still tries not to say too loudly: frontier models are impressive, but the harder product is the industrial choreography underneath them. Someone has to line up land, turbines, substations, cooling, fiber, financing, and a GPU roadmap before your “intelligence layer” can finish one dramatic keynote sentence.

The Cloud Would Like a General Contractor

The most revealing line in KKR’s announcement is that Helix will act as a single coordination point for hyperscalers’ data centers, power, connectivity, and related needs. That sounds boring until you remember how much of the current AI economy is basically a panic attack about who can secure enough capacity first.

This is not KKR buying a cool AI app and pretending private equity discovered innovation. It is KKR looking at the market and noticing that the real scarcity is no longer merely model talent or benchmark bragging rights. The scarcity is everything physical and contractual that sits below the model. Helix plans to invest across hyperscale data center development and operations, baseload and flexible power generation, transmission and distribution, and fiber. In other words, it is packaging the annoying grown-up parts into an actual company.

The plumbing is the point. NVIDIA’s role is not just decorative logo glitter, either. KKR says Helix will support deployment of NVIDIA DSX AI factory-aligned infrastructure with goals including lower total cost of ownership, higher tokens per watt, and faster time to first token. You can practically hear the procurement teams exhale. The AI industry spent two years talking like it was building software and is now talking, much more honestly, like it is building a utility that occasionally writes code.

If that sounds familiar, it should. SiliconSnark has been watching this drift for months. In our look at CoreWeave renting Anthropic more GPUs, the joke was that cloud infrastructure had become premium rental property. In the AirTrunk India buildout piece, the point was that AI increasingly resembles national infrastructure wearing GPU branding. Helix is the cleanest expression of that thesis yet: not just a landlord, but a bundled landlord-power-broker-construction-manager with Jensen Huang at the ribbon cutting.

What Is Actually Smart Here

I am more impressed than annoyed, which is not a sentence I hand out casually to giant capital stacks.

First, the structure makes sense. Hyperscalers do not merely need racks. They need capacity delivered fast enough to satisfy model roadmaps, with enough power certainty to prevent AI strategy from becoming a hostage situation with the local grid. By pairing long-duration capital with an energy partner and NVIDIA’s blueprinting, Helix is trying to reduce the coordination tax. Useful because it makes the whole proposition operational instead of decorative.

Second, the leadership choice matters. Adam Selipsky is not being hired to cosplay as a cloud statesman. He ran AWS through a period when cloud demand became more enterprise-critical and more infrastructure-intensive at the same time. That background fits the problem. Helix is not really a bet on one model vendor. It is a bet that the next five years of AI will reward whoever can turn “we need capacity” into “the transformers are already ordered.”

Third, this story captures the strategic maturity of the market. We are past the phase where every important AI headline had to involve a new assistant persona or a benchmark everyone promises is definitely fair this time. On June 11, the more important signal was that private capital, utilities, chip design, and hyperscale operations are fusing into a more formal stack. As the Financial Times noted in same-day coverage, power and labor shortages are already threatening a meaningful share of data center projects. Helix is, in effect, a company built around that sentence.

The Great AI Rebrand From Magic to Megawatts

The funny part is that the industry still occasionally wants us to talk about AI as if it were mostly about software delight. Reader, it is about substations now.

Helix arrives one day after everyone spent another cycle debating models, agents, and product wars, and then quietly reminds the market that none of those categories scale without industrial inputs. This is why the best current AI stories keep sounding less like app reviews and more like freight financing with delusions of grandeur. Two days ago SiliconSnark wrote about Broadcom, Apollo, and Blackstone turning AI compute into a finance product. Before that, we went deep on Anthropic raising $65 billion to feed Claude the entire power grid. None of these are isolated oddities. They are different camera angles on the same transition.

What Helix understands is that the AI race now has a logistics layer, and the logistics layer is becoming investable in its own right. That has real consequences. It means fewer of the most consequential decisions happen inside the model release notes and more happen inside infrastructure committees, power negotiations, debt structures, and supply contracts. The demo is never the hard part. The hard part is getting 24/7 high-density compute to exist where and when someone wants to bill for it.

The Part That Still Smells Like Capital Fever

Now, the criticism.

Any time a private-equity giant announces a beautifully integrated answer to a structural bottleneck, I become spiritually obligated to check whether the answer is “we discovered a new asset class with better stage lighting.” Helix is more serious than that, but the incentive stack is still worth staring at. AI infrastructure may be one of the defining investment themes of the decade. It is also a category where optimism can stack faster than power lines.

There is execution risk everywhere. Power interconnection queues are real. Construction timelines are real. Community resistance is real. Labor constraints are real. The possibility that AI demand remains huge but less linear than every investor deck implies is also real. Even the smart version of this bet still assumes that hyperscaler urgency, chip roadmaps, energy politics, and financing discipline can coexist for long enough to keep the machine humming. That is a lot of choreography for one logo wall.

There is also a small philosophical problem: when the AI economy starts needing one-stop capital-and-power concierges, it becomes much harder to maintain the fiction that this is just another software cycle. It starts looking like railroads, telecom, cloud, and merchant power had a very expensive child together. Good for the people selling picks, shovels, and electrons. Potentially less charming for anyone who thought “AI competition” would mostly be about elegant research ideas and not whose utility partner got there first.

The Verdict: Real Shift, Not a Vibes Machine

My verdict is that Helix is a real shift, not a vibes machine.

Not because it changes model capabilities tomorrow. It does not. It matters because it clarifies what the category has become. The major AI winners in 2026 are not just the companies with the cleverest models. They are the ones able to secure land, power, financing, deployment speed, and enough political tolerance to build mini-industrial empires disguised as cloud infrastructure.

So yes, KKR launching a $10 billion AI utility starter kit with NVIDIA and Vistra is funny in the way all giant infrastructure headlines are funny. It is also one of the cleanest same-day AI signals we have gotten in weeks. The market is converging on a blunt truth: intelligence is glamorous, but capacity is sovereign. And if you can package the boring parts tightly enough, the boring parts become the product.