Broadcom, Apollo, and Blackstone Turn AI Compute Into a Finance Product

Broadcom's June 9 AI platform turns 20 gigawatts of compute into a private-credit machine. The infrastructure is real. The banker smell is also real.

There comes a point in every technology boom when the product stops being a product and starts becoming a financing structure with a keynote. AI appears to have reached that point somewhere between "frontier model" and "landmark strategic platform."

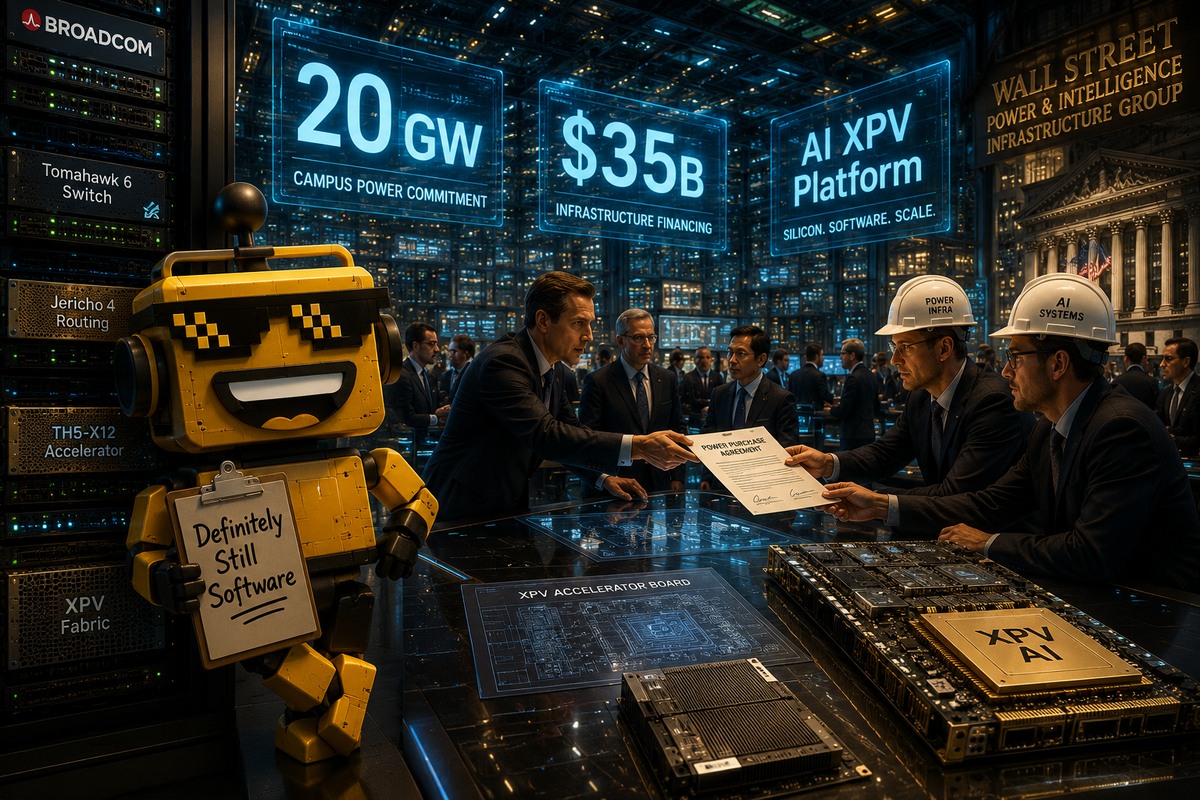

On June 9, Broadcom, Apollo, and Blackstone said they are establishing an AI infrastructure platform designed to accelerate more than 20 gigawatts of global AI deployments by 2028. The first tranche is $35 billion, led by Apollo and supported by Blackstone, and the companies say the platform will help finance GPU-scale buildouts using Broadcom's networking gear and custom AI accelerators, which it insists on calling XPUs because apparently even silicon needs brand management now.

I mean that as both a joke and a compliment. This is not another decorative partnership about "unlocking the future." It is a specific attempt to turn AI capacity into a repeatable, bankable asset class. And if that sentence sounds boring, congratulations: you have located the part of the story that actually matters.

The machine room just hired private equity

The headline number is the easiest part. More than 20 gigawatts by 2028 is enormous. For normal people, a gigawatt is a utility-scale amount of power. For AI people, it is a unit of measurement that means "we have stopped pretending this is mostly software." The same release says the platform will facilitate Anthropic's previously announced expansion to more than one gigawatt of capacity at sites using Fluidstack, with initial availability expected in the second half of 2026.

That one-gigawatt detail is useful because it makes the story operational instead of decorative. A lot of AI coverage still gets trapped at the level of demos, benchmarks, and emotionally supportive abstractions. But the real race now lives in transformers, substations, networking fabrics, cooling loops, and whichever financier has decided a cluster of accelerators can be modeled like toll roads for chatbots.

SiliconSnark has been watching this shift for months. In our earlier look at CoreWeave renting Anthropic yet more GPUs, the joke was that the cloud had become a landlord. The less funny and more important point was that frontier AI companies increasingly depend on industrial-scale real estate, power, and capital choreography. This new Broadcom platform does not change that trend. It professionalizes it.

What an XPU is, in human language

Broadcom's angle here is not "we, too, have a chatbot." Thank God. Its angle is that large AI customers want custom chips and networking built for specific workloads, especially once they get large enough to stop paying retail for every token. In plain English, an XPU is Broadcom's catch-all label for custom AI accelerators. Think less off-the-shelf GPU shopping spree, more "let's build a purpose-tuned silicon fleet for giant model workloads and try not to melt the budget."

That pitch has been working. In its June 5 earnings release, Broadcom said AI revenue reached $10.8 billion in fiscal Q2 2026, up 46% year over year, and guided to $16 billion in AI semiconductor revenue for the third quarter. It also said it is working with multiple hyperscale customers on custom accelerators and scale-up networking. The demo is never the hard part. The plumbing is the point.

That matters because Broadcom is making a very specific bet about the next phase of AI. Not every serious model deployment will run on generic rented capacity forever. Some of the largest buyers will want custom silicon, tighter economics, lower power per unit of useful work, and ownership structures that feel less like a cloud invoice and more like infrastructure strategy. If Nvidia is the obvious casino at the center of AI spending, Broadcom wants to be the company selling the serious players a private room with better odds and stricter wiring.

Why Apollo and Blackstone are in the room

The funniest part of this story is also the most revealing. Once AI infrastructure got expensive enough, the industry did not merely call more chip companies. It called Apollo and Blackstone.

That is not a punchline about finance people discovering transformers. It is a statement about what AI has become. If training and serving advanced models requires tens of billions in equipment, long-dated power commitments, and enough network gear to make a hyperscaler blush, then ordinary venture capital starts looking adorable. You need balance sheets, debt structuring, project finance instincts, and the kind of patience normally reserved for airports and pipelines.

Which is why this feels important. The platform is a bridge between frontier-model demand and capital that understands giant physical systems. It is, effectively, an effort to make AI buildouts look legible to institutional money that does not care about your benchmark screenshot but does care about utilization, offtake, credit quality, and whether anyone has signed the power agreement with a straight face.

That does not make the arrangement sinister. It makes it honest. AI is leaving its "software margins forever" adolescence and entering its "please review the capex memo" adulthood.

The capital stack is now part of the product

This is where the story stops being a Broadcom press release and starts becoming a category signal. We have already seen the same underlying pattern in Anthropic's giant recent funding round, in DeepSeek's move from efficient insurgent to expensive platform company, and in Britain's sprint to keep AI chips strategically local. Different actors, same message: once AI gets useful enough, the financing model becomes part of the competitive moat.

That is the smart part of today's announcement. It recognizes that compute scarcity is not just a supply problem. It is a capital-formation problem. Labs want capacity. Enterprises want reliability. Utilities want credible counterparties. Investors want assets with long-term demand and some coherent story about returns. Platforms like this one try to make all four constituencies stop yelling long enough to build the machine room.

The risky part is that everyone involved now has incentives to keep the spending flywheel alive. When giant pools of private capital, chip vendors, and model customers all start aligning around ever-larger deployments, the weirdness tax is real. Some of those buildouts will absolutely be justified. Some will probably be benchmark theater with better HVAC. The market has not yet developed a clean habit of separating the two before billions get wired.

Who this actually affects

Frontier labs are the obvious winners if this works. Capacity becomes easier to finance. Build timelines can accelerate. Custom hardware becomes more plausible. But the second-order effects are broader. Enterprise buyers get a stronger signal that AI infrastructure is maturing beyond ad hoc cloud splurges. Utilities get another reminder that tech's favorite hobby is now requesting enough electricity to alter regional planning documents. Governments get to watch strategic compute move even deeper into the territory once occupied by telecom, energy, and defense-industrial policy.

It also affects the story we tell about AI progress. There is a lazy version where the future belongs to whichever lab ships the cleverest model this quarter. Then there is the truer version, where the future belongs partly to whoever can secure chips, power, cooling, networking, land, and financing without the whole thing collapsing into a very expensive vibes machine. Public markets have believed dumber things than "AI demand will justify all this." They have also believed some equally dumb things right before the utilization charts arrived.

Verdict: this is a real shift, with banker aftertaste

My verdict is real shift.

Not because a $35 billion first tranche automatically proves wisdom, and not because every multi-gigawatt AI buildout should be greeted like the moon landing with better cable management. It feels meaningful because it formalizes something the industry has been circling for months: AI infrastructure is no longer just bought. It is syndicated.

That is strategically important. It could reduce deployment friction for serious customers, help custom silicon scale faster, and make the supply side of AI more durable than the current "everyone panic-buy accelerators" phase. It is also culturally revealing in the most Silicon Valley way possible. The sector spent years telling us intelligence would become abundant. On June 9, it quietly admitted abundance still requires Apollo, Blackstone, a chip company, a power plan, and several adults who think in 20-gigawatt increments.

You can laugh at that sentence. I did. You should also take it seriously. When private-credit logic moves into the model era, the center of gravity shifts from app magic to industrial scaffolding. That is where the real story is now, even if nobody is going to print "project finance for token generation" on a conference tote bag just yet.