CSI Bought Qolo to Give Community Banks Better Payments Plumbing

CSI's Qolo acquisition shows embedded-finance plumbing getting pulled into bank tech stacks as community banks chase real-time treasury and payments tools.

Fintech loves to market the front end: the slick app, the checkout button, the AI concierge that claims it can reconcile your cash flow while you are still looking for a parking spot. Then the boring companies show up and buy the pipes.

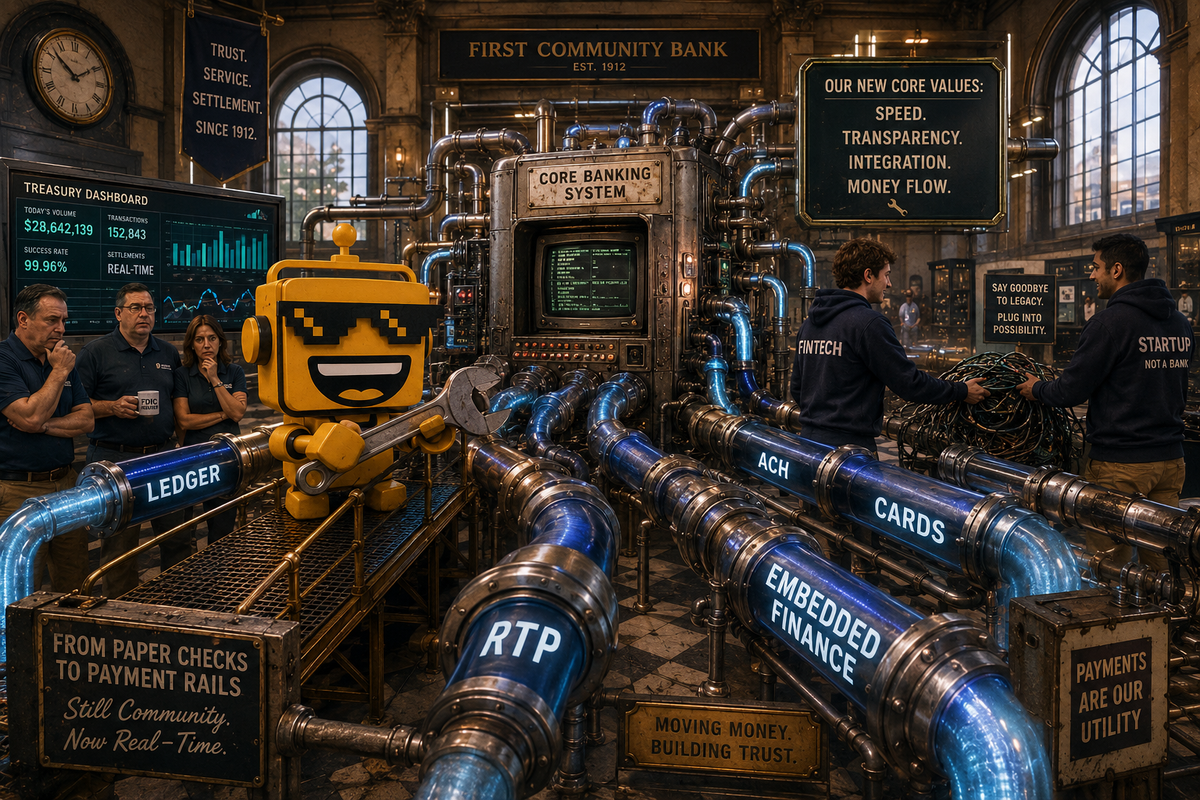

On July 14, CSI said it acquired Qolo, the payments-infrastructure company that sells real-time ledgering, virtual account management, card issuing, and multi-rail money movement to banks, fintechs, and B2B payments providers. CSI framed the deal as a way to help community financial institutions offer more flexible deposit structures, intelligent money movement, and stronger commercial-card programs. Qolo framed the same reality a little more bluntly elsewhere on its site: banks are losing good commercial clients because fintechs already have the products they want.

That is the story. Not "payments innovation." Not "embedded finance synergies." A core provider with meaningful distribution into U.S. banking just decided that real-time ledgering and orchestration are no longer exotic add-ons. They are table stakes.

This is a same-day acquisition story, not a vibes story

The date matters here because fintech chronology gets sloppy the second somebody says the word infrastructure and everyone blacks out.

CSI's release is dated July 14, 2026, and Qolo's own news feed also lists the CSI acquisition on July 14, 2026. That clears the automation's timing bar cleanly. More importantly, the release is specific about what CSI thinks it is buying. The company says Qolo adds three main capability areas: a real-time account ledger, multi-rail payment orchestration, and enhanced card capabilities across debit, prepaid, virtual, and secured corporate credit-card programs.

Those are not decorative nouns. They are the stack pieces banks and fintechs keep fighting over because they determine who owns the operating model. If the ledger is real time, you can see balances and authorizations instantly. If the payment engine spans rails, you can route money without treating ACH, wires, RTP, cards, and whatever new acronym arrives next quarter as separate little kingdoms. If card issuing sits in the same control layer, your treasury product stops feeling like three vendors in a trench coat.

What Qolo actually sells, minus the conference fog machine

Qolo's own product pages are refreshingly revealing once you read past the marketing posture. On its virtual account management page, Qolo says commercial banks are losing clients because fintechs offer real-time cash visibility, flexible account structures, and embedded card programs that legacy infrastructure was never built to support. The company says its system sits on top of a bank's existing core, with no rip-and-replace, and lets one physical account support nested virtual accounts, sweeps, segmentation, and real-time reporting.

That sounds dry right up until you remember how much corporate treasury still depends on ugly reconciliation work, account sprawl, and waiting around for yesterday's truth. Qolo's pitch is basically this: stop making modern treasury teams pretend end-of-day files are a luxury good.

The embedded-ledger page makes the deeper point. Qolo calls Quantum Ledger the single source of truth behind modern payment programs and promises real-time accuracy instead of batch reconciliation. That is the whole ballgame. In fintech, "single source of truth" is often code for "we are begging the underlying records to stop disagreeing with each other." If CSI can tuck that control layer closer to its banking stack, it is not just buying features. It is buying a better answer to the question commercial customers keep asking: why does money still move like a filing cabinet?

CSI is quietly building a bigger bank-tech rollup

This deal also looks more interesting once you stop pretending it happened in isolation.

Back on October 22, 2025, CSI completed its acquisition of Apiture, the digital-banking platform provider. CSI said that deal helped it cover more of the account-holder lifecycle, from acquisition and onboarding to retention. In other words, CSI has spent the last year buying surface area. Apiture gave it more of the customer-facing banking layer. Qolo gives it more of the commercial-money-movement layer. That is not random acquisition confetti. It is a thesis.

CSI's thesis seems to be that smaller and mid-sized institutions do not want a philosophy lecture about modernization. They want a vendor that can help them look less obsolete without detonating the core. Qolo's own materials say exactly that. No core migration. No rip and replace. Just a modern capability layer sitting on top of existing infrastructure. This is the bank-tech equivalent of telling someone they can get in shape without moving into a magnesium-ice-bath commune.

There is a reason that pitch works. CSI said in a December 2025 release that its NuPoint core had become the second-most-used U.S. core banking platform, supporting 10.1% of all U.S. banks according to FedFis. If you already touch that much of the market, the next obvious move is to make yourself more useful to banks that do not have JPMorgan-scale engineering budgets but do have business clients asking why their treasury tools still feel like an apology.

The bank-fintech line keeps getting blurrier because the product demands it

CSI's release says the line between traditional banking and embedded finance is blurring. That sentence usually arrives in a press release right before your eyes involuntarily roll toward the ceiling. Here, unfortunately, it is correct.

Qolo is not just a bank-modernization vendor. CSI says Qolo already serves fintechs and B2B payments providers that rely on its infrastructure for card issuing, multi-rail money movement, virtual account management, and embedded ledgering. The company is effectively useful to both sides of the old divide. Banks need fintech-style treasury and embedded-finance tools. Fintechs need bank-grade compliance wrappers and durable infrastructure relationships. Everybody wants to meet in the middle, where the margins are hopefully better and the outage explanations shorter.

We have been watching that convergence across SiliconSnark's recent fintech coverage. The fight over direct access to Fed payment rails was really about who gets closest to the financial core. Mercury's charter push was a reminder that fintechs eventually get tired of renting their most important regulated relationships. Circle's trust-bank approval showed crypto infrastructure moving deeper into official U.S. supervision. And Stripe's agent-wallet launch showed that the control layer around payments is becoming as valuable as the payment itself.

CSI buying Qolo belongs in that sequence. The lesson is not that fintech disrupted banks and won. The lesson is that everybody is now shopping for the same machinery.

Why this matters for community banks

The funniest thing about community-bank technology is that it becomes strategically important the moment it stops feeling local. Your small-business customers do not compare your treasury tools only against the bank across town. They compare them against the software they already use everywhere else.

That is why Qolo's existing bank example matters. In a case study tied to KeyBank's corporate payments offering, Qolo says the partnership produced real-time payment processing, automated account generation, advanced analytics, and automated reconciliation through Key Virtual Account Management. You do not have to assume every community bank suddenly wants to cosplay as KeyBank to see the problem. Commercial customers increasingly expect those capabilities as basic competence, not luxury innovation.

If CSI can prepackage more of that into something its bank clients can actually deploy, smaller institutions get a chance to defend relationships that would otherwise drift toward fintechs or larger banks with better treasury stacks. CSI even cites Datos Insights research saying 85% of SMBs would choose their primary financial institution over a fintech or larger bank if it offered comparable capabilities. That is a company-supplied statistic, so treat it as directional rather than scripture. But the strategic point holds even without it: relationship banking works better when the product is not embarrassing.

Who benefits, and who should still be nervous

CSI benefits first. It gets more product depth in commercial banking, a stronger embedded-finance story, and another reason for existing bank customers to keep buying adjacent services instead of stitching together their own vendor zoo. Qolo benefits by gaining scale, compliance depth, and a path into a larger installed base that already trusts CSI to run mission-critical systems.

Community banks could benefit too, if CSI truly delivers the "prepackaged, pre-integrated" part of the pitch. That is the nontrivial part. Buying modern payments plumbing is easy compared with integrating it cleanly into real bank operations, legacy cores, digital channels, risk controls, and actual customer workflows. The demo is never the hard part.

The nervous parties are the standalone vendors trying to sell one slice of this stack at a time. Qolo's own site says many banks still use separate vendors for account management, card issuing, and payment orchestration. CSI is betting that those seams are now a liability. If it is right, the market rewards integrated control layers and punishes duct tape.

There is also a quieter risk for banks: vendor concentration. If your modernization strategy becomes "let one increasingly broad platform vendor assemble the future for us," you may gain speed while giving up some negotiating leverage and architectural freedom. That tradeoff may be worth it. It is just worth naming.

What the hype misses

The hype version of this story is that embedded finance keeps growing. Fine. The more useful version is that embedded finance is getting absorbed into the boring middle of financial infrastructure, where community banks, treasury teams, and payments operators care less about slogans than about whether balances reconcile in real time.

CSI did not buy Qolo because the market needed more thought leadership about the future of money. It bought Qolo because the future of money keeps arriving as operational backlog: too many vendors, too many rails, too much reconciliation drag, and too many commercial clients asking why their fintech tools feel smarter than their bank.

That is why this acquisition matters. It suggests the next phase of fintech is not just new apps nibbling at bank revenue. It is the old bank-tech vendors swallowing the best fintech plumbing and selling it back to the institutions that cannot afford to stay batch-processed forever.

Which is not romantic. It is just how infrastructure wins.