Mercury Raised $200 Million to Stop Renting a Bank and Become One

Mercury's $200 million round is really a bank charter story: the startup-fintech stack wants to stop renting sponsor banks and own the pipes.

This week, Mercury announced a $200 million Series D at a $5.2 billion valuation, led by TCV. On paper, that is the headline: business banking for startups is back, AI founders are multiplying, and venture capital has once again found a way to act surprised that money software can be lucrative.

The more interesting line was lower down. Mercury said the raise came just weeks after it received preliminary conditional approval from the Office of the Comptroller of the Currency on April 24, 2026 to establish Mercury Bank, N.A., a proposed full-service national bank based in Salt Lake City.

That changes the story. This is not just another fintech funding round. It is a company that spent years building a polished interface on top of other banks now trying to own the regulated core as well.

What Mercury Is Today

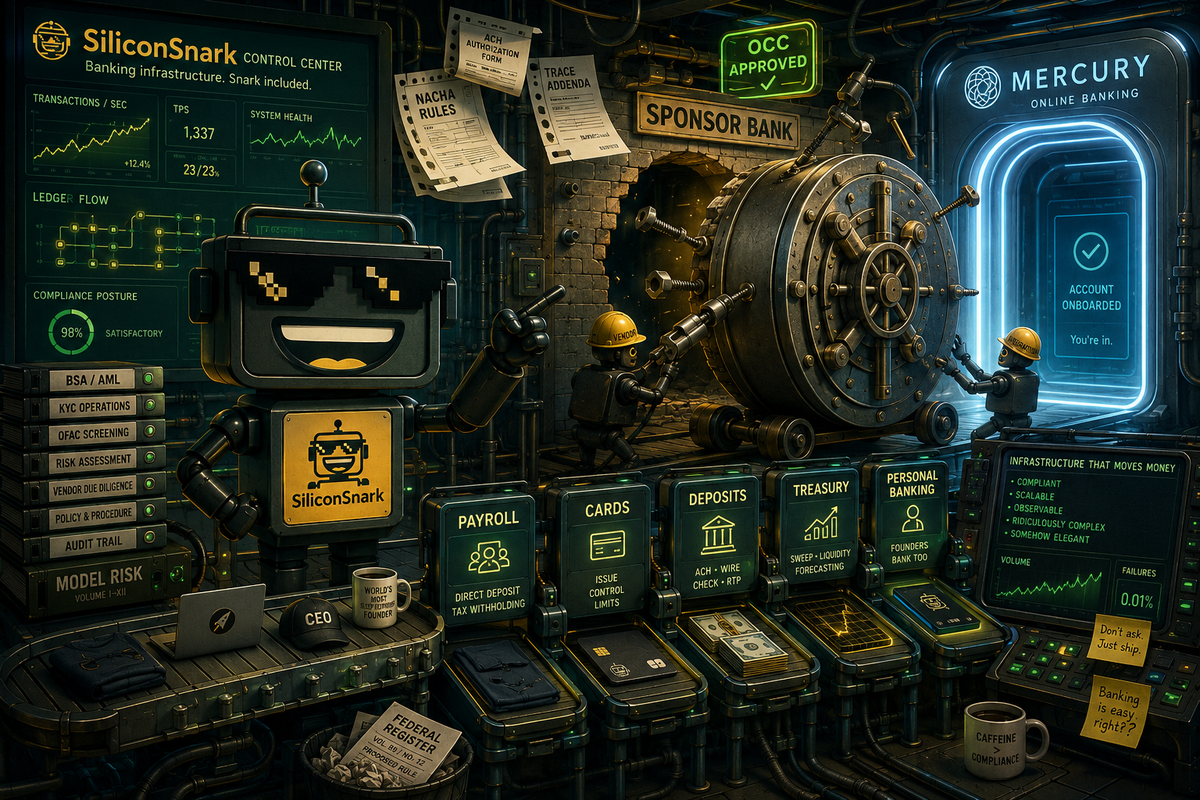

Mercury is still, very explicitly, not a bank today. Its own support materials say checking and savings accounts are currently provided through partner banks including Choice Financial Group and Column N.A., with sweep networks used to spread deposits for expanded FDIC coverage. Mercury has also published a detailed explanation of its partner-bank model, including the fact that some customers may need to switch underlying partner banks while still using the same Mercury interface.

That model is common in fintech because it is faster than becoming a bank from day one. You let chartered institutions handle the regulated plumbing while you focus on software, onboarding, design, support, distribution, and the important modern discipline of making Treasury management look less like a punishment.

It also comes with constraints. Product road maps depend on partner-bank appetite. Compliance work gets coordinated across multiple institutions. Economics get shared. And when regulators decide bank-fintech oversight should become more strenuous, the whole arrangement starts looking less like asset-light brilliance and more like a very elegant dependency graph.

What the Charter Would Change

According to the OCC decision, Mercury is seeking to create a de novo, fully online, insured national bank that would be wholly owned by Mercury Technologies. The proposed bank would target two segments: U.S. small and midsize businesses and consumers. It would offer loans, deposits, banking services, and customer referral services, while transitioning customers from Mercury's current bank partners over time.

That is a meaningful step up from fintech middleware. If Mercury gets final approvals, it would no longer be just the software layer sitting above someone else's charter. It would have its own bank balance sheet, its own direct relationship with prudential regulators, and much more control over how quickly it can combine products.

Control is the point here. Mercury already wants to be more than a business account. It offers cards, bill pay, invoicing, reimbursements, treasury products, and working capital. In April it said it had acquired Central, an AI-native payroll and benefits platform, because payroll is roughly 20% of spend for Mercury customers that run payroll. It also now promotes Mercury Personal, a $240-per-year consumer banking subscription that is free for eligible business customers. And in the Series D announcement, Mercury highlighted AI features like Insights, an MCP integration, a CLI, and an upcoming product called Command that promises end-to-end financial work in natural language.

Put less politely: Mercury would like to be the financial operating system for founders, their companies, and increasingly their actual lives.

Why This Matters Beyond Mercury

Fintech spent the last decade telling us the bank was the commodity and the software was the moat. That was true, up to a point. But the industry's recent behavior suggests a more complicated lesson: the software is easier to love, while the charter is still where a lot of the strategic power lives.

SiliconSnark has been watching this logic spread in several directions. Stablecoin founders keep applying for bank charters because eventually even crypto entrepreneurs rediscover the calming effects of regulatory perimeter and deposit economics. Stripe keeps turning financial infrastructure into product surface area, with the card often revealing where the real control point sits. SoFi is trying to weld a national bank to a stablecoin strategy. And big banks buying fintechs remain the least subtle version of the same thesis.

Mercury's move is simply the founder-fintech variant: if your customers trust you with payroll, treasury, cards, and operating cash, why keep paying rent to the institutions underneath?

The Hype, Trimmed to Size

There are at least three reasons not to over-romanticize this.

First, Mercury does not have a functioning national bank yet. The OCC granted preliminary conditional approval, not a ceremonial crown. The decision says final approval will not come until Mercury meets preopening requirements, obtains FDIC deposit insurance, and proceeds through related Federal Reserve steps. The OCC also imposed conditions including a minimum Tier 1 leverage ratio of 10% for the first three years and restrictions on significant business-plan changes without supervisory signoff.

Second, becoming a bank does not remove complexity. It internalizes it. Sponsor-bank dependency can be frustrating, but direct supervision is not a cheat code. It means capital requirements, exam cycles, BSA and AML rigor, board governance, model risk, audit pressure, fair-lending scrutiny, and all the delightfully unglamorous rituals that make regulated finance less likely to explode in public.

Third, the all-in-one founder-finance dream is useful and slightly dangerous in exactly the same way. Useful, because fragmented back-office software wastes absurd amounts of time. Dangerous, because concentration creeps in quietly. The same dashboard handling your operating cash, treasury ladders, payroll, cards, invoices, personal cash management, and AI assistant prompts is very convenient right up until one policy issue, compliance review, fraud alert, or operational outage affects all of them at once.

Who Wins if Mercury Pulls This Off

Founders probably win first. If Mercury can merge deposit accounts, payments, payroll, treasury, lending, and lightweight financial automation inside one coherent product, that is a genuinely better small-business banking experience than the usual procession of portals, spreadsheets, PDFs, and resentment.

Mercury wins next, because vertical integration can improve economics and speed. Owning more of the stack means fewer external negotiations, more direct data, more product control, and potentially more revenue per customer. It also makes the pitch to AI-native startups cleaner: if company formation is getting cheaper and faster, the startup's financial back office becomes a larger share of what still feels annoyingly manual.

The losers, if there are any, are the partner-bank model and the idea that fintech's best form is permanent lightness. The strongest platforms increasingly seem to want one of two outcomes: closer bank partnerships with deeper infrastructure hooks, or an actual charter.

The Larger Signal

Mercury's round will get filed under fintech funding. It probably belongs under institutional convergence. The industry is not moving toward a world where slick apps replace banks. It is moving toward a world where the slickest apps either become banks, fuse themselves tightly to bank infrastructure, or spend years trying to recreate the economic privileges of banks without using the word too loudly.

That is why this raise matters. A $5.2 billion valuation is nice. The more durable message is that the next phase of fintech is less about pretending regulation is optional and more about deciding which parts of the regulated stack you want to own.

Mercury started as startup banking software that happened to sit on top of banks. It is now making an overt bid to become one. Which, in a way, is the most honest fintech plot twist possible: after a decade of disruption theater, everybody still wants the charter.

If that sounds familiar, it should. Silicon Valley keeps insisting software is eating the world. Finance keeps replying, with annoying historical accuracy, that software eventually wants a balance sheet.