Stablecoin Founders Keep Applying for Bank Charters, Because Apparently the Endgame Was Banking All Along

OCC stablecoin rules and a growing bank-charter queue show crypto’s next act is less anti-bank rebellion, more reserves, audits, and supervision.

For years, crypto sold itself as the thing that would route around banks. Then it met payroll, enterprise treasury, compliance, redemption windows, payment finality, and the basic human preference for money that still exists when the app refreshes. Suddenly the revolution started filling out charter paperwork.

That is the more revealing fintech story right now. On March 2, the Office of the Comptroller of the Currency published its proposed stablecoin rulebook implementing the GENIUS Act, with comments due by May 1. And as of April 22, the OCC’s own digital-asset licensing page lists 12 pending applications, including filings from OpenReserve, Revolut, Morgan Stanley Digital Trust, zerohash, and World Liberty Trust Company.

This is not a vibe shift. It is a business-model confession. If you want to issue dollar-like liabilities, manage reserves, promise redemption, and persuade institutions that your token is not just a very polished science project, you do not actually want to abolish finance. You want a better seat inside it.

The Rulebook Is the Hook

The proposed OCC framework matters because it turns stablecoin regulation from general aspiration into operating detail. The President’s Working Group report from November 1, 2021 argued that Congress should create a comprehensive federal framework for payment stablecoins. New York’s Department of Financial Services then filled part of the vacuum with June 8, 2022 guidance requiring full reserve backing, par redemption, and regular attestations for supervised dollar-backed issuers. In March 2025, the OCC also pulled back from several Biden-era crypto risk statements and said banks could continue custody, reserve, and payment activities under ordinary supervision, provided they do the boring risk-management work.

Now the boring work has names and deadlines. Under the OCC proposal, nonbank state-qualified issuers that cross the $10 billion outstanding issuance threshold face a federal transition process unless they win a waiver. The proposal also spells out expectations around redemption policies, reserve disclosures, capital, operational resilience, customer protection, and information-security controls, including testing for systems and smart contracts. In other words, the government has arrived with a clipboard.

That clipboard is not anti-innovation. It is a recognition that a stablecoin is basically a promise wearing better UX. The entire product depends on whether the market believes the issuer can redeem on demand, safeguard reserves, survive a cyber incident, and avoid discovering too late that “programmable money” is still quite programmable by fraudsters, counterparties, and bugs.

Even Treasury’s latest international messaging points in the same direction. In the April 8, 2026 joint statement from the U.S.-UK Financial Regulatory Working Group, officials said they discussed regulation that would support the adoption of stablecoins for payments. That is a subtle but important tell. The policy conversation is no longer “should this exist at all?” It is “under what supervisory conditions do we let this plug into actual finance?”

The Charter Queue Is Telling on the Industry

The OCC’s applications page reads like a casting call for crypto’s regulated adulthood. OpenReserve Bank, N.A., received by the OCC on April 13, is applying as a de novo national bank in Utah with FDIC insurance. Its public filing explicitly references stablecoin risk management, GENIUS Act compliance, and even tokenized deposit and on-chain settlement operations. That is not “move fast and break things.” That is “move carefully and please let us into the payments system.”

Revolut Bank US, N.A., filed on March 4, wants a de novo national bank that would transition Revolut’s existing U.S. activities into a federally supervised banking entity. That application matters because Revolut is not approaching the charter question as crypto cosplay. It is approaching it as distribution. The super-app era keeps rediscovering the same lesson: if you already have customers and a broad financial-services ambition, the bank charter stops looking like overhead and starts looking like infrastructure.

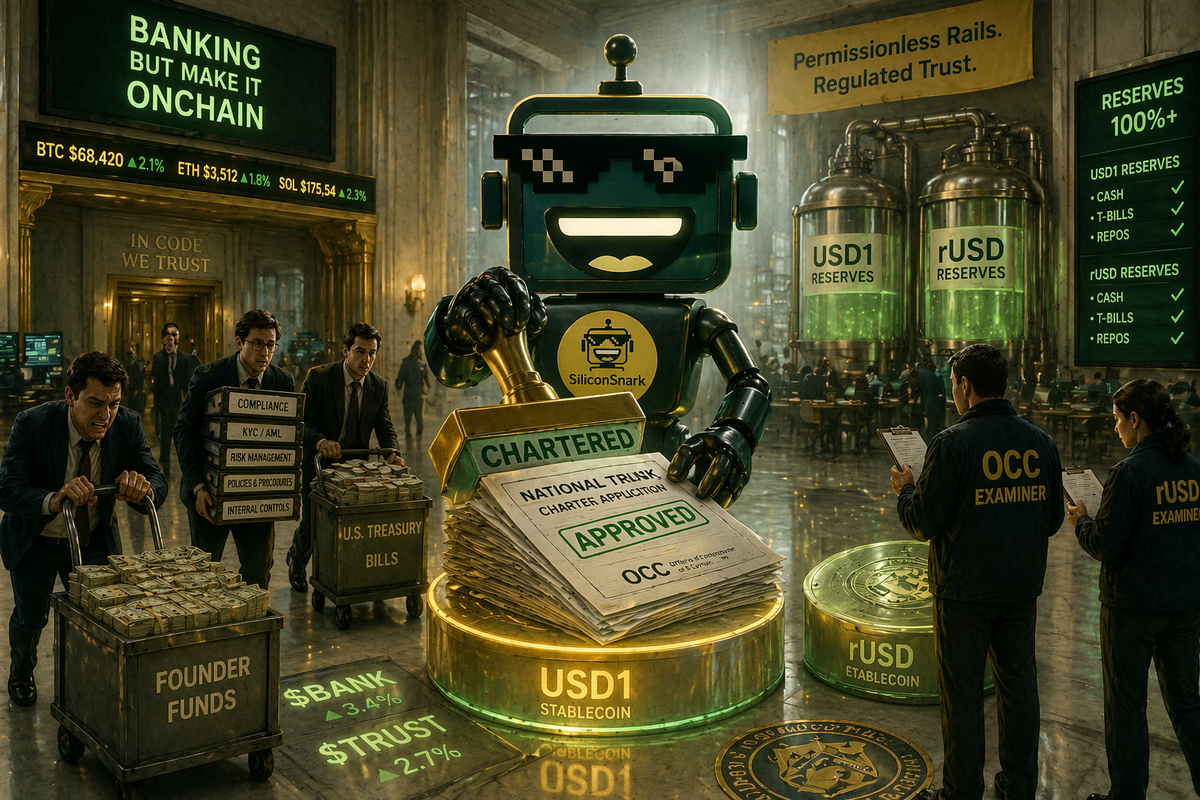

Then there is World Liberty Trust Company, whose January 5 application proposes a non-insured national trust bank in Miami that would issue the USD1 stablecoin, manage reserves, and provide institutional custody. The filing is unusually explicit: it says the trust company would issue a fiat-backed digital asset designed to maintain a one-to-one value with the U.S. dollar and hold reserves in deposits, government money-market funds, and cash equivalents. Whatever you think of the sponsor, the strategic logic is obvious. If the product is a dollar promise, then regulatory legitimacy is not a side dish. It is the entree.

The broader pattern is what matters. Some applicants want insured bank status. Some want trust-bank structures. Some want custody, some payments, some issuance, some a cleaner bridge between tokenized liabilities and plain old regulated balance sheets. But nearly all of them are converging on the same answer: the fastest way to make digital dollars respectable is to make them look institutionally familiar.

What a Charter Actually Buys You

A bank or trust charter does not magically make a stablecoin good. It does make the issuer easier to supervise, easier to audit, and easier to understand. It can clarify who is responsible for reserve management, redemption, custody, consumer disclosures, cybersecurity, and governance. It can also reduce the awkwardness of trying to build a payment product while describing yourself as adjacent to the banking system but absolutely not of it, which is a bit like opening a restaurant and insisting you are merely adjacent to food.

This is why the current stablecoin moment fits so neatly with other trends SiliconSnark has been tracking. Visa’s USDC settlement push was not really a crypto story so much as a treasury and settlement story. PayPal’s Pix expansion in Brazil was a reminder that the winning payment rail is usually the one that already works at scale. XFX’s pitch around stablecoin-to-fiat plumbing is fundamentally about making conversion less painful. And SoFi’s crypto move inside a national bank showed how quickly “crypto adoption” turns into a question of which regulated wrapper customers trust enough to tap.

All of these stories point to the same conclusion. The killer app for stablecoins is not ideological purity. It is operational usefulness inside systems that still care about reconciliation, dispute handling, sanctions screening, and not getting a 7 a.m. call from a regulator.

Who Wins, Who Is Exposed

The winners here are the issuers that can afford adulthood. Large platforms, well-capitalized operators, and firms with enough legal budget to treat supervision as a moat all benefit when the market shifts from “launch a token” to “run a regulated institution.” That does not guarantee success, but it does filter out some of the tourist traffic.

Consumers and enterprise users could also benefit, at least in theory, from clearer redemption rights, better reserve transparency, more explicit governance, and stronger operational controls. A stablecoin that lives under meaningful supervision is still risky, but it is a more legible kind of risky. There is value in knowing which entity owes you the dollar, which assets back the promise, and which regulator gets very annoyed if the answer turns out to be “it’s complicated.”

The exposed group is everyone who mistook adoption for inevitability. Smaller issuers may find that compliance, capital, cybersecurity, and reporting costs are not a minor nuisance but the whole game. Banks that dismissed stablecoins as a passing crypto side quest may also discover that payments modernization is happening anyway, only now it is being packaged in bank-shaped wrappers. And regulators themselves are exposed to a subtler risk: if the framework becomes too cumbersome, activity can migrate offshore or into structures that preserve the economics of stablecoins while dodging the supervision that makes them tolerable.

There is also the very old-fashioned risk that everyone becomes too enchanted by the wrapper. A charter does not eliminate concentration risk in reserve assets. It does not eliminate governance problems. It does not eliminate run dynamics if confidence breaks. It does not eliminate smart-contract or infrastructure vulnerabilities. It just means the resulting mess is more likely to happen in a venue with examiners, remediation plans, and very expensive lawyers.

What the Hype Still Misses

The hype keeps pretending the stablecoin battle is between brave crypto natives and stubborn legacy finance. That framing is increasingly useless. The real contest is over who gets to become the new regulated middleware for moving dollars, settling transactions, and holding reserve assets. Some of those winners may come from crypto. Some may come from banks. Some will come from whichever company is most willing to sound revolutionary in public and deeply conventional in its risk committee.

There is nothing hypocritical about that. Payments is a scale business built on trust, and trust is expensive. The market keeps rewarding firms that can borrow credibility from regulation, bank partnerships, reserve quality, and operational discipline. The crypto industry spent a decade learning that code is not a substitute for institutional confidence. Fintech spent a decade learning that elegant front ends eventually collide with the ugly middle of money movement. Stablecoins now sit directly in that overlap.

So yes, the charter queue outside the OCC is a little funny. It is also the clearest sign yet that stablecoins are maturing from a crypto category into a financial-infrastructure category. Once that happens, the job is no longer to sound disruptive. The job is to clear compliance, manage reserves, survive scrutiny, and make users forget how much machinery is hiding behind the tap-to-pay moment.

That may be less romantic than the original white papers promised. It is, however, how products become real.