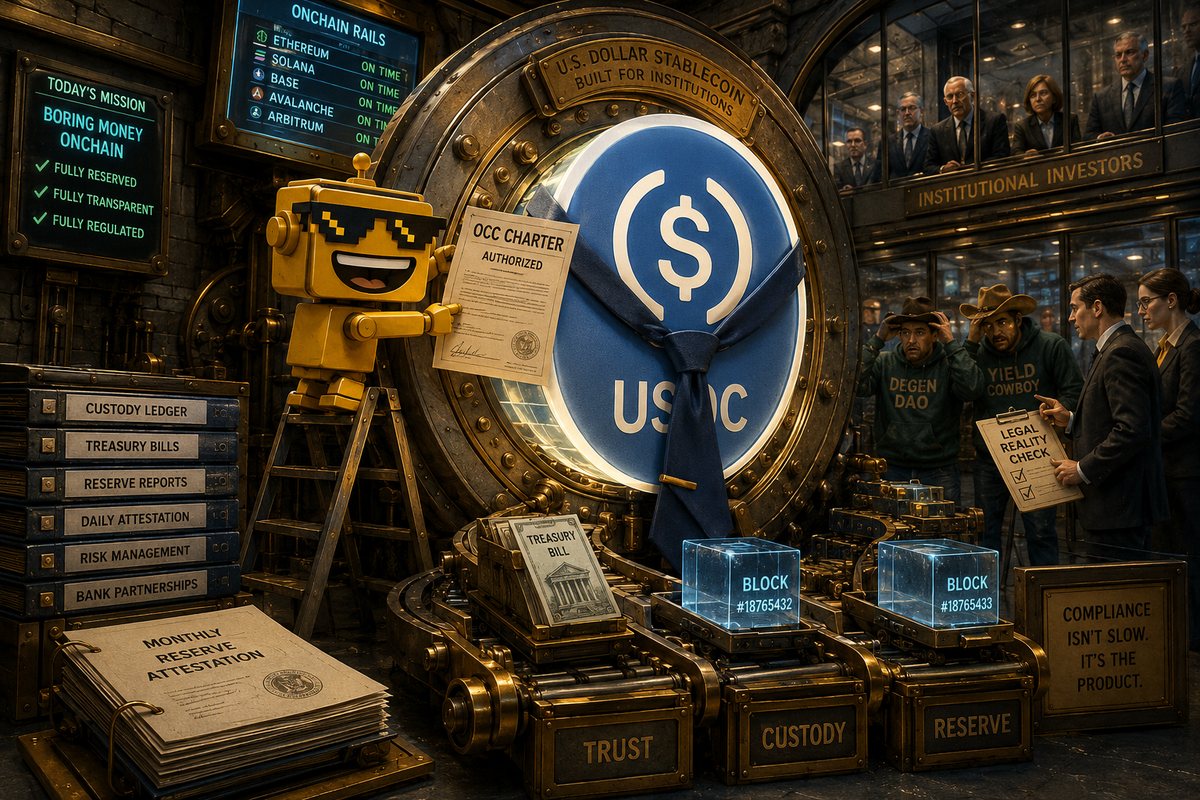

Circle Got a Trust Bank for USDC and Made Crypto Wear a Tie

Circle's new OCC-approved trust bank pulls USDC deeper into the federal perimeter, proving stablecoin ambition now looks less bankless and more chartered.

Stablecoins spent years marketing themselves as the part of finance that would finally stop asking permission. Then one of the category's biggest winners went and got a bank charter.

On July 10, Circle said it received final approval from the Office of the Comptroller of the Currency to establish First National Digital Currency Bank, N.A., which will operate as Circle National Trust. The company's description is careful and instructive. Upon opening, the new entity will provide fiduciary digital-asset custody services for Circle and its affiliates, with the option to offer limited institutional custody later, and the charter is designed to support future reserve-management capabilities for USDC under federal oversight.

That is the headline. The real story is what kind of victory this actually is. Circle did not become a normal consumer bank with checking accounts, branch lollipops, and an app that asks whether you would like to round up spare change into ETFs. It became a national trust bank. That sounds narrower because it is narrower. It also matters more than it sounds, because the plumbing is the point.

This is not a crypto company escaping regulation

The chronology matters because fintech stories get sloppy the moment people start treating charter approvals like vibes.

Circle applied for the charter on June 30, 2025. The OCC then granted conditional approval on December 12, 2025 for First National Digital Currency Bank, alongside approvals for Ripple, BitGo, Fidelity Digital Assets, and Paxos. Circle's July 10 announcement says the company has now received final approval, after spending the intervening months moving from "promising applicant" to "federally approved trust-bank operator."

That sequence is the opposite of deregulated chaos. It is crypto infrastructure moving deeper into the regulated perimeter on purpose. Circle is effectively saying the future of stablecoins will not be won only with APIs, liquidity, and issuer scale. It will also be won with prudential credibility, custody authority, and a federal supervisor who can walk in and ask unpleasantly specific questions.

If you have been reading SiliconSnark on Circle's managed-payments push for institutions that would rather not touch crypto directly, this move feels like the next logical step. Circle is building toward a world where stablecoins are not a speculative sidecar. They are a regulated service layer for payments, settlement, and treasury operations, with enough adult supervision to make large institutions stop flinching.

What a trust bank actually is

This is where the story gets more interesting than the phrase "bank charter" usually implies.

In a February 2026 proposed rule on national bank chartering, the OCC said national trust banks are national banks whose operations are limited to those of a trust company and related activities. The agency said it currently supervises approximately 60 national trust banks, and that the majority are uninsured. The same proposal also notes that trust banks frequently conduct custody and safekeeping activities and collectively hold nearly $2 trillion in custody or safekeeping accounts.

Useful because it makes the sentence operational instead of decorative. Circle National Trust is not some mystical hybrid creature that has transcended old finance. It is joining a very real regulatory category with a real history, a real supervisor, and a fairly specific institutional job description. Trust banks are good at safeguarding assets, administering fiduciary responsibilities, and doing serious back-end work. They are not simply "normal banks, but onchain."

That distinction matters because fintech loves collapsing different regulatory identities into one triumphant press-release noun. "Bank" is a powerful word. In practice, the difference between a full-service bank, an industrial loan company, a trust bank, a partner-bank arrangement, and a money-transmitter stack is the difference between very different economics, powers, obligations, and risks. We saw that in Mercury's effort to stop renting a bank and become one. We saw it again when the fight over direct Fed payment-rail access exposed how much strategic value still sits near the regulated core.

Why Circle wants this so badly

The optimistic version is straightforward. Circle wants USDC to be the trusted digital dollar infrastructure for institutions that care about regulation, transparency, and operational continuity more than they care about cosplay. A federally supervised trust-bank wrapper helps. It gives Circle a sturdier answer to every nervous treasury team, bank partner, and policymaker asking the same question in different accents: what exactly happens around the reserve, the custody stack, and the legal claims if this thing gets systemically important?

Circle's July 10 release is explicit that reserve management is planned as a future capability. That means the company is trying to bring more of the USDC operating core into an OCC-regulated entity over time. The company framed that as improving the safety, transparency, and trust of USDC. Fair enough. But it also gives Circle more direct control over the infrastructure that matters most once stablecoins stop being a crypto product and start becoming treasury substrate.

This is the same broader convergence SiliconSnark has been tracking across the stablecoin scramble among banks, card networks, and fintech platforms, and in big banks building tokenized deposits to keep stablecoins from eating treasury work. Everyone wants software-like money movement. Nobody wants to surrender the trusted account relationship, compliance wrapper, or settlement economics. Circle's charter win is what that competition looks like when a stablecoin issuer decides the best way to stay disruptive is to become harder to dismiss.

The bigger signal is not Circle alone

Today's news also lands in the middle of a larger licensing queue that is starting to look less like an exception and more like a migration.

The OCC's current digital-assets licensing list, updated through late June, includes applicants such as Catena Trust Bank, Payward National Trust Company, Agora National Trust Bank, OpenReserve Bank, EDX Trust, Revolut Bank US, zerohash national trust bank, PAYO Digital Bank, and World Liberty Trust Company. That is a strange sentence if you still think modern fintech's endgame is permanent life outside the banking perimeter.

It is a very normal sentence if you have accepted that many fintechs eventually rediscover the old institutional privileges: direct supervision, clearer legal status, better control over infrastructure, and the ability to stop subleasing key parts of the business from someone else. Public markets have believed dumber things than "the bankless revolution keeps applying to become adjacent to a bank."

The Federal Reserve's own research has been moving in parallel. In a March 30, 2026 FEDS Note, Fed researchers wrote that Congress passed the GENIUS Act in July 2025 to create a regulatory framework for payment stablecoins and argued that payment stablecoins could reduce certain frictions in cross-border payments by lowering reliance on traditional intermediary chains. That was not a meme-coin sermon. It was the central bank politely acknowledging that parts of the stablecoin thesis are economically real.

Circle's trust-bank approval is what happens when a company tries to operationalize that reality inside an official U.S. regulatory category instead of forever hovering around it.

Who benefits, and who should still be cautious

Circle benefits first. It gets legitimacy, a stronger institutional sales story, a clearer custody setup, and a path toward bringing more reserve-related activity into a federally supervised structure. That is valuable not just for optics, but for business development with banks, asset managers, exchanges, payment companies, and global enterprises that would like the speed of public blockchains without treating governance as an optional accessory.

USDC's institutional users probably benefit too, at least in the sense that the infrastructure beneath them gets more legible. A trust bank is not magic, but it is a familiar supervisory object. In fintech, familiar supervisory objects are underrated product features.

The people who should stay cautious are the ones who hear "bank" and assume the old consumer protections travel automatically with the word. A national trust bank is still a different beast from a normal insured retail bank. The OCC's own proposed-rule discussion says most national trust banks are uninsured, and Circle's charter is about custody and related trust activities, not some grand reinvention of household banking. This is a story about financial infrastructure becoming more regulated, not about every stablecoin suddenly behaving like a checking account with patriotic wallpaper.

There is also the concentration question. The more stablecoin infrastructure moves into a handful of heavily licensed, heavily connected players, the more the category starts looking like conventional finance with better uptime and stranger nouns. That may be healthy. It may also mean the upside accrues to the firms best positioned to industrialize compliance, custody, and policy relationships, while the open, messy, permissionless romance gets quietly escorted toward the service elevator.

What the hype misses

The hype version says Circle just proved crypto is winning. The more accurate version is sharper and funnier. Circle just proved that one durable way to win in crypto is to become easier for regulators, banks, and institutions to live with than the word "crypto" would normally suggest.

This is not betrayal. It is maturation. The same market that once pitched stablecoins as an escape hatch is increasingly pitching them as a better-operated dollar layer for payments, settlement, collateral, and treasury flows. In that world, the weirdest flex is not sounding unregulated. It is sounding dependable.

Circle did not turn into JPMorgan. It did something more revealing. It put one of the largest stablecoin businesses in America into a federal trust-bank suit and asked the rest of the market to admit that maybe the future of fintech is not "no banks." Maybe it is "different banks, narrower charters, and much more software."

Which, in fairness, is still a plot twist. It is just a very regulated one.