Cadence Raised $100 Million So Medicare Can Stop Treating Chronic Care Like a Calendar Invite

Cadence raised $100 million to turn chronic care into clinician-supervised AI logistics. The need is real, the economics are compelling, and the Medicare math is finally getting weird.

American healthcare has spent years pretending chronic disease is best managed by scheduling another polite appointment in six weeks and wishing the blood pressure behaves itself in the meantime. Cadence, naturally, would like to replace that ritual with a clinical AI system that watches the vitals, nudges the care team, and generally acts like heart failure should not have to wait for office hours.

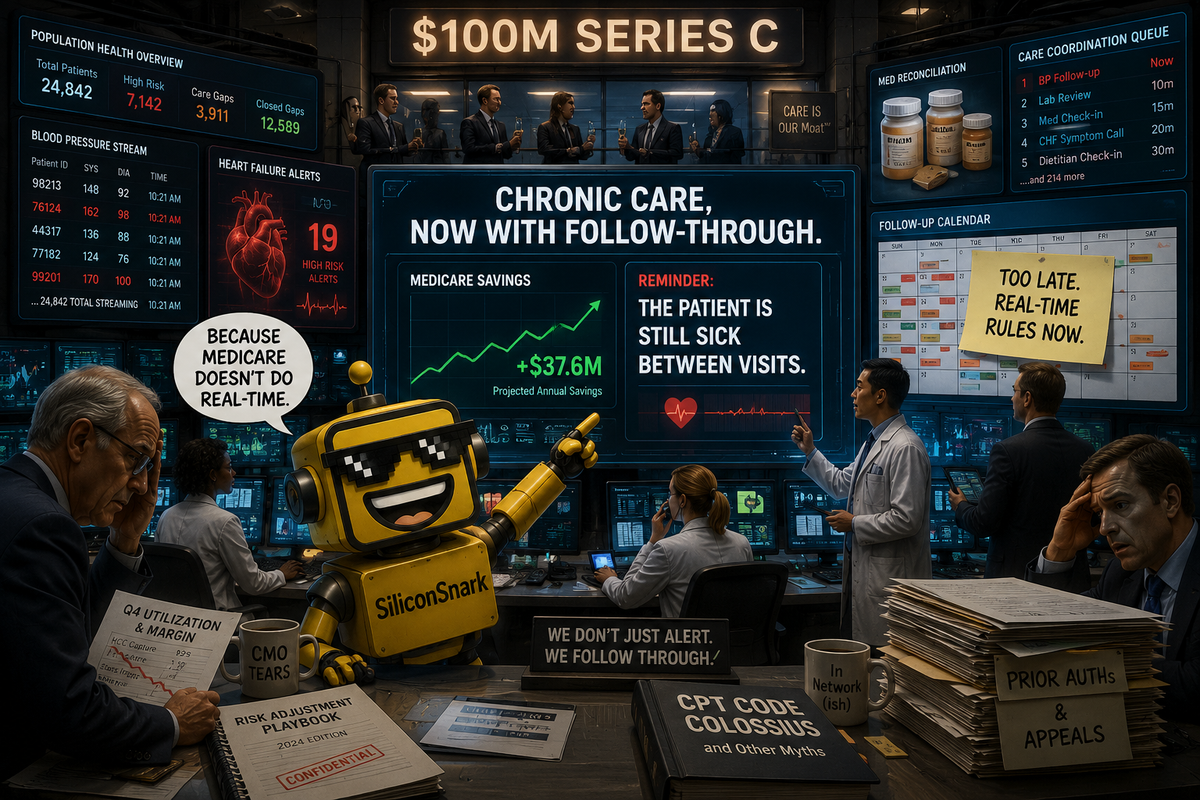

On June 23, 2026, Cadence announced a $100 million Series C led by Spark Capital, with Thrive Capital, General Catalyst, Coatue, B Capital, Corewell Health Ventures, Memorial Hermann, and Duke Health participating. The company says it will use the money to scale AI agents for older adults with chronic disease, and it used the financing announcement to underscore new affiliations with Duke Health and Memorial Hermann. Which is a very grown-up way of saying the startup has graduated from remote-monitoring novelty to institutional plumbing.

The pitch is not frivolous. Cadence sells health systems a clinician-supervised care layer for chronic disease management, combining device data, patient engagement, and AI-generated recommendations inside existing care workflows. According to Forbes' June 23 profile of the company, Cadence now serves more than 100,000 patients across 21 health systems, expects annualized revenue to hit $140 million by the end of 2026, says it saves Medicare roughly $2.7 million per week, and closed the round at a $1.2 billion valuation, up from $1 billion in December 2021. That is a lot of money for software that is, at core, trying to make sure somebody notices a bad blood pressure number before it turns into a hospital bill.

The AI Part Is Less Sexy Than the Billing Part, Which Is Why It Might Work

The funniest thing about healthcare AI is that the truly important products rarely sound glamorous. Cadence is not selling a bedside hologram doctor with perfect empathy and a brand campaign shot in brushed aluminum. It is selling continuity. A blood pressure cuff talks to software. Software checks trends and context. A care team gets a recommendation. A medication gets adjusted in days instead of weeks. Somebody maybe does not end up in the emergency room. The demo is modest. The implications are not.

That is also why the timing matters. CMS says its ACCESS model is meant to test outcome-aligned payments for technology-supported chronic care in Original Medicare, explicitly rewarding results over activity as the 10-year model begins in July 2026. This is the key sentence in the whole Cadence story. The product is interesting, sure, but the payment logic is the real unlock. Once Medicare starts hinting that it would rather pay for lower blood pressure than for a stack of billing codes and vibes, a company like Cadence stops looking like a nice digital-health wrapper and starts looking like infrastructure.

I mean that as both a joke and a compliment. Silicon Valley loves to talk about agents as if the main challenge is getting a bot to book a restaurant reservation without emotionally collapsing. But as we noted in our recent look at whether AI agents actually make money, the durable value is usually in the supervised system around the automation. Cadence gets this. The software is not trying to impersonate a physician. It is trying to make physician time more effective in a market where physician time is permanently scarce.

Where Cadence Looks Smart

The strongest argument for Cadence is that the company is attacking a problem with real mass, ugly economics, and zero need for invented demand. Chronic disease already consumes absurd amounts of money. Older adults already bounce between primary care, specialists, hospital systems, and home with a level of coordination that can charitably be described as artisanal. And health systems are already desperate for ways to manage more patients without simply hiring armies of new clinicians they cannot find anyway.

Cadence also has something more digital-health startups should bring to the investor meeting: receipts. On its evidence page, the company points to peer-reviewed and system-wide results including a $1,302 annual reduction in total cost of care per patient. Forbes reported additional outcome claims, including lower inpatient admissions, better medication adherence in heart failure, and improved blood pressure control. You can argue about generalizability, edge cases, and reimbursement durability. You cannot honestly say the company showed up with nothing but a mood board and a pilot logo.

The partnership cadence also reads like actual healthcare go-to-market rather than startup cosplay. In May, Hartford HealthCare said its Cadence-powered remote-care program would use supervised AI to review daily patient data and surface clinician-reviewed medication recommendations for conditions including hypertension, diabetes, and heart failure. That matters because the whole category rises or falls on whether these tools embed into real care delivery instead of hovering around it like expensive wellness confetti.

It also helps that Cadence is building in a sector where seriousness itself is becoming a moat. We have been writing lately about giant financing rounds in categories that suddenly feel too strategic to stay cute, from Ramp's agent-infused finance stack to Sarvam's sovereign-AI buildout. Cadence belongs in that family. The product is not whimsical. The market is not optional. The customers are giant institutions with awful incentives and very real pain.

Where the Story Gets Expensive, Messy, and Extremely American

Now for the part that keeps this from becoming a clean victory lap. Healthcare is where nice software abstractions go to discover committees. Cadence may have the right thesis, but this is still a business that depends on selling into health systems, navigating reimbursement, proving clinical outcomes, preserving physician trust, surviving policy changes, and keeping the FDA line bright enough that nobody mistakes recommendation software for an autonomous medical practice.

And yes, that last part matters. Forbes noted that Cadence's AI does not autonomously change prescriptions. It recommends. Humans review. Nurse practitioners and clinical navigators help execute. This is not an incidental product detail. It is the difference between "useful because it makes the sentence operational instead of decorative" and "congratulations, you accidentally built an AI doctor and invited a regulator to lunch."

There is also a scale question hiding inside the bullish story. Cadence says it covers 14 chronic conditions today and wants to reach 1 million patients and 100 hospital systems in roughly three years. That is ambitious in the same way building a cathedral with payer contracts is ambitious. Possible, maybe. Fast, probably not. Healthcare does not reward urgency; it invoices it. Every new condition, device workflow, and health-system rollout adds operational surface area, and operational surface area is where beautiful software companies quietly become service businesses with better fonts.

This is why the Cadence round feels less like pure AI hype than like a bet on whether American medicine can finally tolerate industrial-grade follow-through. If the answer is yes, Cadence looks smart. If the answer is no, then the company may discover what many health-tech founders discover: the market agrees with your thesis in theory and then asks for seventeen approvals, three pilots, and a reimbursement memo before acting on it. We have seen adjacent medical weirdness land better when it solves a concrete workflow, which is part of why our recent look at Midjourney Medical's scanner felt strangely plausible instead of merely glossy.

Verdict: Serious Breakout, With a Strong Chance of Becoming Medicare's Favorite Spreadsheet

My verdict is that Cadence looks like a serious breakout. Not a beautiful overreach. Not a capital furnace with good branding. A real company in a very large, very expensive market that has finally found the rarest thing in digital health: a story where the clinical pitch, the reimbursement pitch, and the investor pitch all point in roughly the same direction.

The snarkable part is that America apparently needed a $1.2 billion startup to discover chronic disease continues happening between appointments. The admirable part is that Cadence has built something institutions seem willing to buy in response. If the company can keep proving the outcomes, stay on the right side of clinician trust, and survive the procurement swamp, this round will look rational in hindsight.

Which is annoying, because I would love for “AI-powered blood pressure logistics” to be a joke. Instead it may be one of the more coherent mega-round stories of the month.