Taktile Raised $110 Million So Banks Can Let AI Touch the Scary Buttons

Taktile raised $110 million to automate high-stakes banking and insurance decisions. The pitch is serious, the controls matter, and the weirdness tax is real.

The most ambitious sentence in fintech this week was not about a crypto moonshot or a neobank for dogs. It was Taktile announcing a $110 million Series C on June 24 so banks and insurers can hand more of their underwriting, onboarding, fraud, claims, and compliance work to AI agents without also handing regulators a reason to schedule a meeting.

This is later-stage money for a very specific kind of startup ambition. Growth Equity at Goldman Sachs Alternatives led the round, with Balderton Capital, Index Ventures, Tiger Global, Y Combinator, and Dig Ventures participating. Taktile says it will use the capital to expand its AI decisioning tools for banks and insurers and grow across the U.S., EMEA, and Latin America. In other words, the company just raised a hundred and ten million dollars to become the adult supervision layer for financial institutions that would like AI to do more than summarize a memo.

That sounds niche until you remember how much expensive human labor in finance is basically structured judgment wrapped in policy, forms, and mild dread. Taktile's thesis is that a lot of this can now be automated if the model is boxed in by rules, context, logging, and humans who can still yank the cord. I mean that as both a joke and a compliment.

Finance Finally Found an AI Use Case It Can Invoice

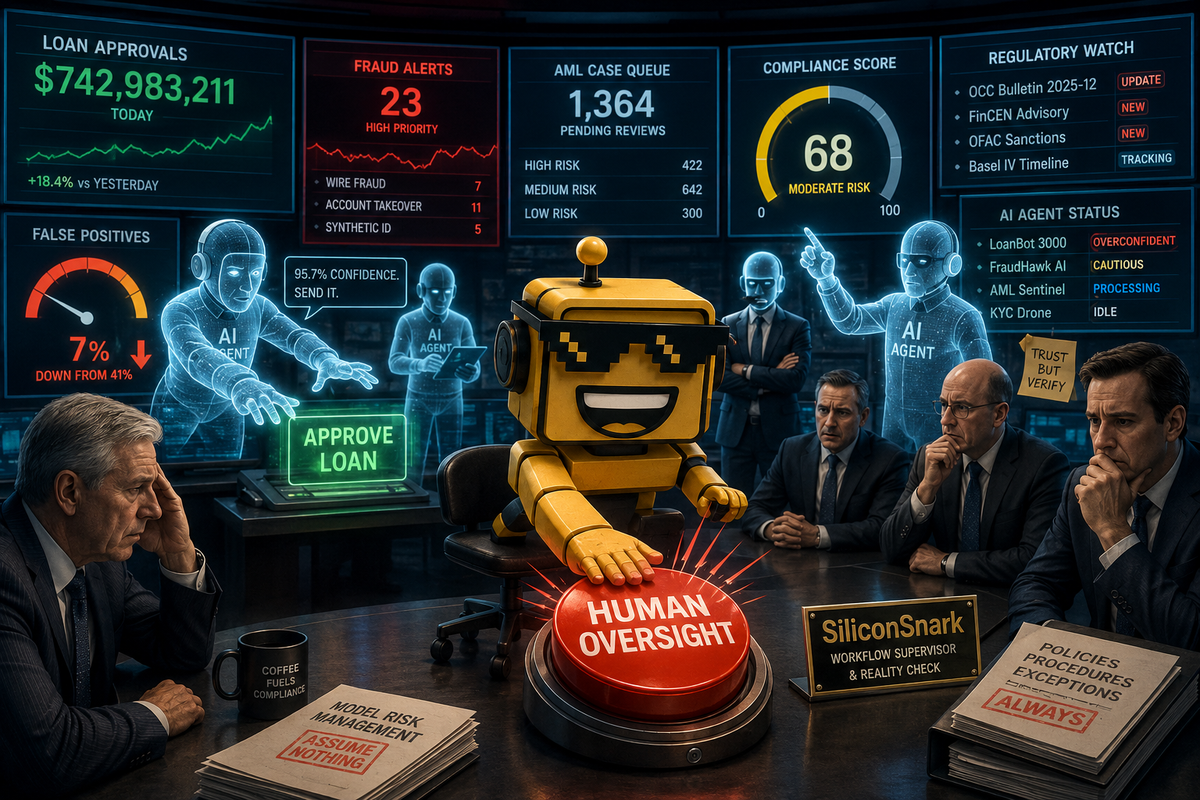

Taktile is not trying to become your friendly chatbot banker. It sells what it calls an agentic decision platform for financial institutions. That means banks, fintechs, and insurers can combine AI agents, business rules, data sources, and human oversight to make operational decisions faster. The company's own examples are revealingly unsexy: approve more business loans, assess claims, onboard customers, catch financial crime, and stop wasting specialists on repetitive reviews. This is not vibe coding. This is workflow trench warfare.

The company says it already powers millions of decisions a day for customers including Mercury, Monzo, Faire, and Pleo, and claims outcomes like 95% automation in B2B underwriting and 75% fewer AML false positives. It also says one large insurer using the platform expects more than $90 million in claims-processing efficiencies. Those are the kinds of numbers investors suddenly become willing to hear all the way through. If you have been following SiliconSnark's ongoing fascination with software agents getting closer to the company card, Taktile is attacking the same macro trend from the opposite side of the ledger: not spending money autonomously, but deciding who gets it, who gets reimbursed, and who gets flagged before someone calls legal.

The Buzzword Stack Is Annoying. The Product Logic Is Not.

I have now read enough AI-fintech copy to recognize the genre where a startup says "agentic transformation" and expects applause. Taktile uses the language too. But beneath the phrase fog, the product logic is unusually coherent. Banks and insurers do not merely want a model. They want a system that can enforce policy, track inputs, explain outputs, escalate exceptions, and let a risk team intervene before a bad automated decision turns into a PowerPoint apology.

That is why this round feels more serious than the average AI funding lap. Taktile is explicitly selling constrained autonomy. It is telling financial institutions they can move faster without pretending regulation is optional. That puts it in the same family as Mastercard's recent attempt to give AI agents a payment rail plus a hall monitor and Collibra's pitch that enterprises need a panopticon for agents. Every credible AI infrastructure story in 2026 eventually becomes a story about guardrails, logging, permissions, and who gets blamed when the robot improvises.

Taktile's own materials say business owners from heads of credit to fraud officers need to understand and control AI-driven decisions. That is useful because it makes the category operational instead of decorative. We are talking about whether an institution can automate a claims queue, an onboarding flow, or a commercial underwriting process and still prove, after the fact, that it did not lose its mind.

Goldman Did Not Lead This Round for the Vibes

Goldman Sachs Alternatives joining this round is not just logo garnish. It is a signal that big-money investors increasingly think the durable AI opportunity in finance sits inside the drab but lucrative machinery of decision-making, not the chatbot layer. Goldman's press release also made the use-of-proceeds unusually clear: Taktile will invest in more product depth for banking and insurance and expand geographically. That matters because this market is not won by shipping a pretty interface and calling it a platform. It is won by surviving procurement, integration, audit questions, regional compliance nuance, and the ancient enterprise ritual known as "we love this, now please talk to twenty-seven stakeholders."

There is also a macro reason this round makes sense. Taktile cites industry data showing financial institutions spend an average of $72.9 million a year on KYC and AML operations alone. Whether or not every bank is ready to let AI touch the scariest buttons, every bank is absolutely ready to lower the labor bill attached to repetitive, highly structured reviews. If you can cut false positives, speed approvals, and leave an audit trail behind, you are no longer selling science fiction. You are selling margin.

The Weirdness Tax Arrives Right on Schedule

Now for the fun part: this entire category is one long negotiation with risk. If an AI agent recommends the wrong credit outcome, who owns it? If an automated claims workflow becomes too aggressive, who unwinds the damage? If a fraud model becomes faster and more confident in a dumb direction, does the institution catch it before customers, regulators, or journalists do?

SiliconSnark has already spent time on what happens when financial distribution starts moving into chat interfaces and on the increasingly recursive business of using AI to babysit other AI. Taktile sits exactly where those threads meet the balance sheet. It is what happens when the agent economy graduates from answering questions to making decisions that can cost real money in the real world.

The risk, of course, is that every company in this space now sounds like it wants to be the operating system for regulated judgment. Some will be feature bundles with confidence issues. Some will get trapped in pilot purgatory. Some will discover that "expand globally" is a much cuter phrase before local rules, legacy cores, and cautious banks enter the chat. And because Taktile did not disclose its valuation publicly, the market still gets to perform the classic late-stage venture trick of sounding extremely confident while leaving one important number offstage.

Verdict: Serious Breakout Energy, With Enterprise Shoes On

My verdict is that Taktile looks like a serious breakout candidate, not a capital furnace with good typography. The company is aimed at a real, expensive bottleneck; the use case is concrete; the customers are legible; and the investor roster makes sense. Most importantly, the product appears built around the actual objection financial institutions have, which is not "can AI do this at all?" but "can AI do this without creating a fresh category of regret?"

That means the next phase of AI in finance may be decided not by whoever talks the loudest about disruption, but by whoever makes automated judgment feel safest, fastest, and least embarrassing in front of a regulator. Taktile just raised $110 million to compete for that job. That is a very large bag of money for software whose core promise is, essentially, "yes, the machine can help, and no, it will not color outside the lines unsupervised." In 2026, that counts as romance.