PayPal Made Wallet Funding Weird Enough for the FCA

The FCA's PayPal wallet probe spotlights who controls checkout when cards, bank accounts, and digital wallets all want to be the front door.

This week, the UK's Financial Conduct Authority said it is investigating Mastercard, PayPal, and Visa under Chapter I of the Competition Act 1998, and Mastercard and Visa under Chapter II, over suspected anti-competitive conduct linked to the funding and usage of PayPal's digital wallet. One day earlier, in its first-quarter 2026 Form 10-Q, PayPal disclosed that it had received notices of investigation and requests for information from the FCA in March 2026 regarding provisions in its contractual agreements with Visa and Mastercard tied to the funding and use of the wallet.

That sequence matters. March was the notice. May 5 was the company disclosure. May 6 was the regulator confirming the probe in public. And the FCA was careful to say it has reached no conclusions and made no findings that competition law was broken.

Still, this is an unusually revealing fintech story because it is not about some moonshot token, AI checkout hallucination, or another executive discovering that "agentic commerce" sounds good on a stage. It is about the least glamorous but most important question in payments: when you tap, click, or autofill your way through checkout, who actually decides which rails get used, who pays whom, and who gets to stand between the consumer and the merchant collecting rent on convenience?

What the FCA Is Actually Looking At

The official FCA statement is terse, but not vague. The agency says it is investigating suspected anti-competitive conduct linked to the funding and usage of PayPal's wallet. The legal framing matters too. Chapter I covers anti-competitive agreements or concerted practices. Chapter II covers abuse of a dominant position. The FCA said it is still gathering evidence and may or may not later issue a statement of objections.

PayPal's own disclosure is slightly more concrete. Its 10-Q says the inquiry concerns certain provisions in PayPal's contractual agreements with Visa and Mastercard relating to wallet funding and usage. In plain English, the regulator appears interested in whether the terms that govern how cards fund PayPal and how that wallet gets used may have distorted competition.

That may sound niche. It is not niche at all. It is the operating system of modern digital payments.

Why Wallet Funding Is Such a Big Deal

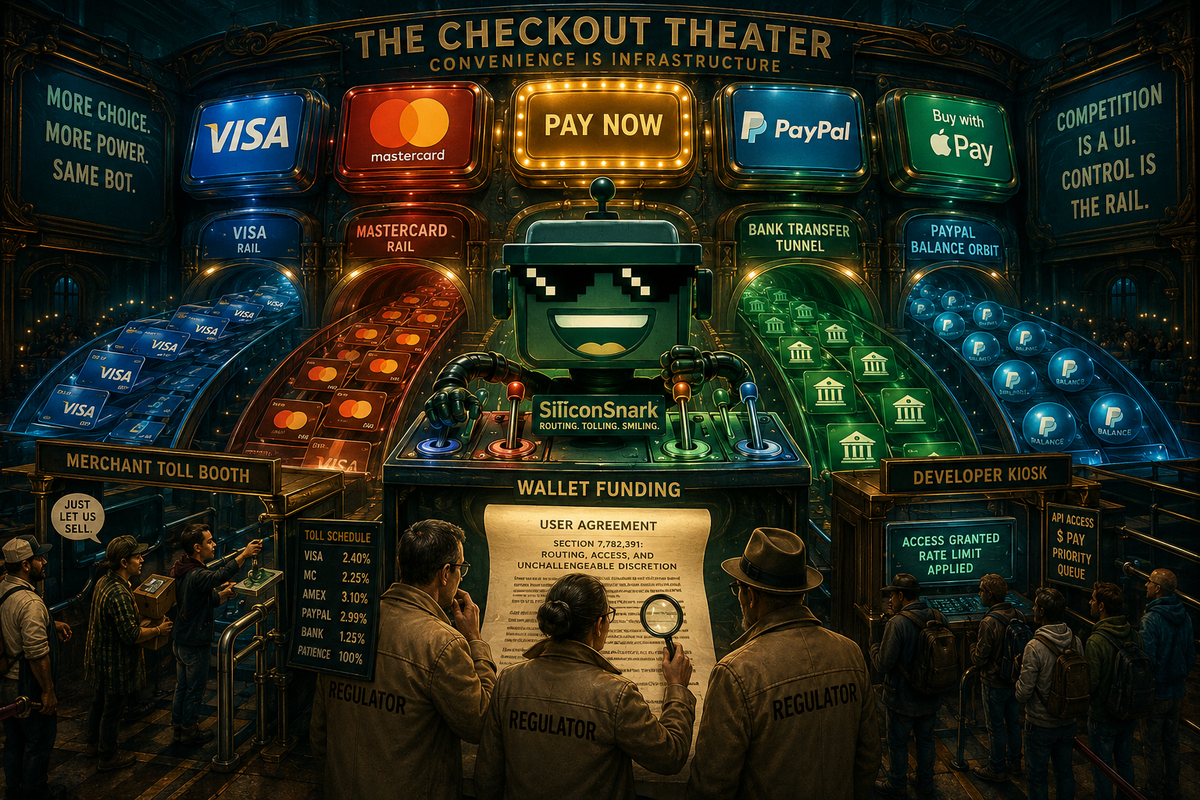

PayPal is not just a button. It is a wallet that can sit in front of multiple payment sources and decide how money enters and exits the experience.

PayPal's own consumer materials say users can add cards and bank accounts to the wallet, including Visa and Mastercard cards, and can also add money to a PayPal balance through linked funding sources, direct deposit, transfers, or cash load options in the U.S. That sounds simple because the interface is supposed to sound simple. Underneath it sits a messier hierarchy of cards, bank transfers, stored balance, merchant acceptance rules, network economics, dispute rights, and commercial agreements.

The FCA and Payments Systems Regulator laid out a helpful framework in their February 2025 digital-wallet feedback statement. They distinguish between pass-through wallets, such as Apple Pay and Google Pay, which do not hold funds themselves and instead tokenize cards, and staged wallets, such as PayPal, which can hold funds and let payment happen in two stages. The same report lists PayPal as a wallet that can hold funds, use cards and bank transfers, and charge merchants rather than card issuers.

Which means PayPal is doing something more commercially interesting than a pass-through wallet. It is not merely presenting your card in prettier clothes. It is deciding how much of the payment experience can be internalized inside PayPal before the rest of the financial system gets invited back into the room.

The Wallet Layer Is Where Competition Gets Weird

The fintech fantasy was always that digital wallets would make money movement cleaner, cheaper, and more competitive. Sometimes they do. They also create a new chokepoint.

If a wallet becomes the consumer's default front door, then the battle shifts upward from the card itself to the interface that chooses among cards, bank accounts, wallet balances, rewards logic, and fallback payment methods. The consumer sees convenience. The merchant sees conversion. The networks and the wallet operator see a negotiation over routing, fees, preference ordering, and data.

This is why the FCA and PSR have been watching the wallet market so closely. Their 2025 report said the share of card transactions using a digital wallet in the UK rose from 8 percent in 2019 to 29 percent in 2023. It also said about 20 percent of UK card users used a digital wallet for more than half of their card transactions in 2023. That is no longer a side feature. That is distribution power.

Usually, the policy conversation has centered on Apple Pay and Google Pay because those pass-through wallets sit inside mobile operating systems and can steer a huge amount of in-store behavior. But PayPal matters for a different reason. It sits closer to e-commerce checkout, can hold money itself, and can shape how cards and bank transfers compete inside its own environment.

What the Probe May Signal, Even Before It Resolves

The fair reading is not that the FCA has proved some grand wallet cartel by Thursday. It has not. The fair reading is that regulators have moved from generalized concern about digital-wallet power to an actual case focused on a specific wallet, specific contractual provisions, and specific relationships with the two dominant global card networks.

That shift matters because fintech's favorite trick is to describe infrastructure choices as product design. Sometimes they are. Sometimes "preferred funding experience" is just a polite way of saying the commercial plumbing was arranged to favor one rail over another.

If regulators decide that wallet agreements can entrench network power, restrict funding options, or shape usage in ways that blunt competition, then the implications travel well beyond PayPal. They touch every company trying to become the default money interface without becoming a full-stack bank, card network, or both.

That is the broader pattern SiliconSnark keeps running into. PayPal's Pix move in Brazil showed a global wallet conceding that the local rail can become the actual product. Stripe's latest Treasury push showed how quickly better rails become account products. Visa's USDC settlement effort was another reminder that incumbents modernize when the back-end economics get too obvious to ignore. And the recent stablecoin charter scramble underlined the same truth from the other direction: everybody eventually wants more control over the money stack.

Who Benefits if the Rules Change

Merchants would like more leverage, or at least fewer mysterious toll booths hidden behind a frictionless checkout button. Alternative payment methods would like a better chance to compete inside the wallet instead of being politely escorted to the side door. Consumers would probably enjoy more competition if it produced cheaper payments or more transparent funding choices, though most users will never voluntarily learn what a staged wallet is and should not have to.

The companies with the most to lose are the ones whose economics improve when the wallet layer can quietly steer behavior. That does not just mean PayPal. It includes any player that benefits when the customer relationship becomes sticky enough to make funding hierarchy, routing, and default choices feel inevitable.

What the Hype Misses

The hype version of fintech says competition happens because a new app appears. The real version is harsher. Competition happens only if the new app does not rebuild a private gate on top of the old rails.

That is why this story is more interesting than another generic antitrust headline. The FCA is not asking whether digital wallets are cool. That question was settled years ago. It is asking whether the contractual machinery behind a very large wallet may have made the market work less well than it could.

And that is a worthy question, because wallets have become too central to be treated like decorative UX. The FCA and PSR said in February 2025 that digital wallets are now an increasingly important touchpoint between large technology firms and UK consumers. Once you become the touchpoint, you stop being just a feature. You become policy.

The Broader Fintech Signal

The signal here is not "PayPal is in trouble," at least not yet. The signal is that regulators are getting more specific about where power sits in payments. Not just at the bank, not just at the card network, not just at the operating system, but in the software layer that mediates all three while calling itself convenience.

That should make the entire sector slightly less comfortable. It should also make the conversation better. Because if fintech wants credit for making money movement cleaner, faster, and more competitive, it should also be willing to explain exactly how its defaults, funding rules, and commercial agreements shape the market. Preferably before the regulator asks in writing.

For now, the facts are simple. In March 2026, PayPal received FCA notices. On May 5, PayPal disclosed them. On May 6, the FCA confirmed a formal Competition Act investigation into PayPal, Visa, and Mastercard tied to the funding and usage of PayPal's wallet. No conclusions yet. But the question on the table is a good one, and fintech rarely enjoys those.