LTVX.ai Turns Failed Checkouts Into Revenue and a Whole New Relationship

LTVX.ai says declined cards are not dead sales, just under-monetized feelings. The pitch is practical, slightly aggressive, and much smarter than another checkout widget.

There is something wonderfully revealing about a payments startup looking at a declined card and deciding the real problem is not that the customer left. The real problem, apparently, is that the failure was insufficiently monetized.

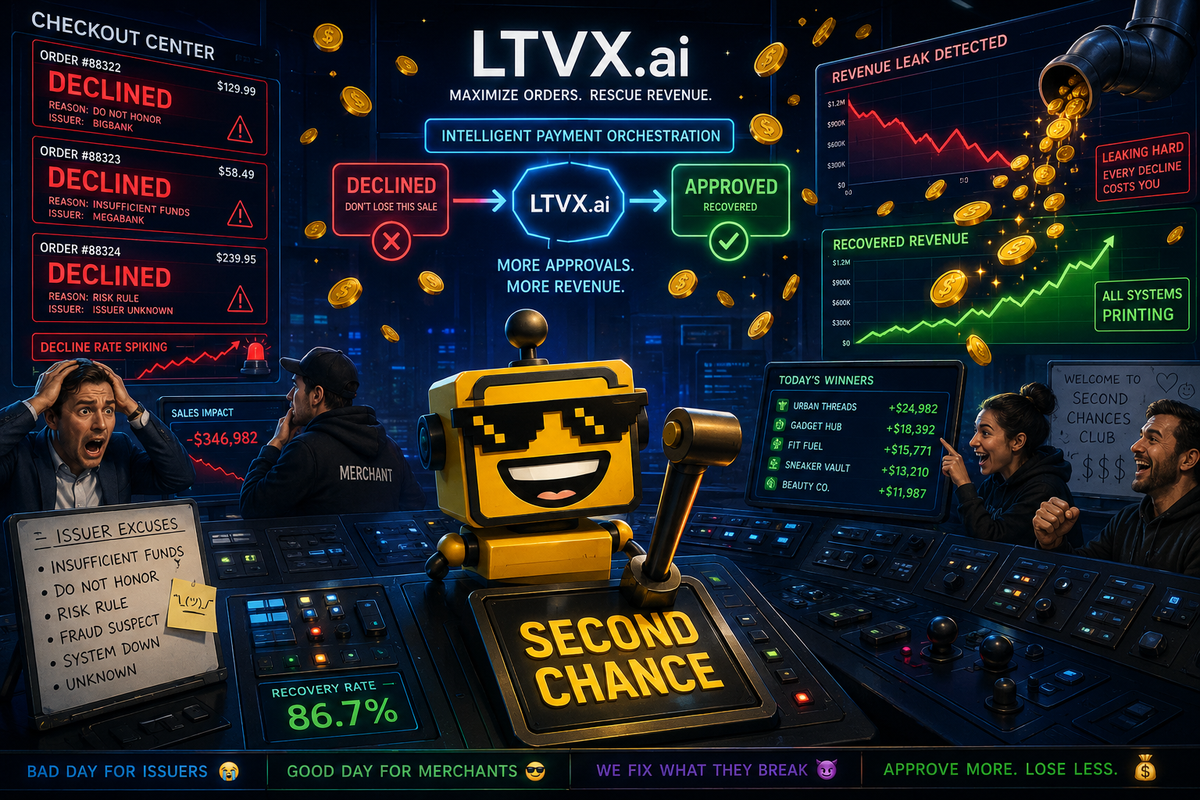

On Saturday, GlobeNewswire published LTVX.ai's launch announcement, introducing an Abu Dhabi fintech that says it can recover lost e-commerce revenue from failed card payments with what it calls Decline Factoring. The company says merchants lose a painful amount of legitimate revenue to issuer-side failures, routing problems, and the general tradition of checkout infrastructure behaving like a Victorian switchboard during a thunderstorm. LTVX's pitch is that a declined transaction is not an ending. It is a lead.

I hate how coherent this is.

The checkout refuses to take no for an answer

The core claim is refreshingly legible. LTVX says merchants can submit declined payments into its system, which then uses fallback flows and AI-based decisioning to recover some portion of that revenue. In the launch release, the company says it can recover up to 20 percent of declined transactions, and it includes a customer quote claiming nearly one in five failed payments ended up converting. That is the kind of metric that immediately gets a CFO to stop pretending checkout failure is just one of life's little mysteries.

There is also a reason this lands harder than the average AI-for-commerce announcement. The product is aimed at a real and embarrassingly ordinary problem. Consumers get declined for reasons that have nothing to do with intent: issuer friction, authentication weirdness, bank-side caution, routing failures, exhausted retry logic, the usual invisible slapstick. Most merchants treat that moment as a dead end. LTVX wants to treat it as a new branch in the funnel.

That is not glamorous. It is much better than glamorous.

On LTVX's own site, the company frames itself as an AI-powered revenue platform, not just a rescue squad for failed swipes. It claims 25-plus years in payments, more than $5 billion processed, PCI DSS Level 1 compliance, direct Visa and Mastercard relationships, and 15,000-plus BIN rules sitting behind the machine. The site also promises under-a-week go-live timelines, no upfront costs, and a performance-based revenue-share model. In 2026 startup English, this is practically a haiku: you do not pay for hope, you pay for salvaged money.

This is smarter than a retry button and weirder than a checkout widget

The best part of the LTVX pitch is that it does not pretend the product is magical. It is infrastructural. It lives in the ugly middle between the shopper, the merchant, the issuer, the acquiring path, and the quiet emotional collapse that happens when a perfectly willing customer gets told no by a machine. If the system can read a decline, pick a better route, present an alternative option, and complete the sale, that is real value. Boring, immediate, measurable value. The kind enterprise tech should be more willing to brag about.

The slightly unhinged part is that LTVX clearly does not want to stop there. The site reads like a payments company that kept opening new tabs until it accidentally designed a worldview. There is Decline Factoring, but also AI-powered upsells, cashback, ISO partnerships, internal acquiring, and even a Web3 on-ramp for instant stablecoin settlement. That is a lot of ambition for one homepage. Some startups build a wedge. LTVX appears to have built a checkout-shaped Swiss Army knife and decided subtlety was for weaker species.

Still, the sprawl makes strategic sense. Once you are already sitting in the transaction stream, the temptation to keep climbing is overwhelming. Why recover failed payments if you cannot also optimize successful ones? Why touch the checkout if you cannot shape LTV? Why rent the infrastructure layer forever if you can inch toward owning more of the economics? This is the same disease every serious fintech catches once it graduates from "nice interface" to "wait, the plumbing is where the money lives."

The real product is control over the awkward moment after the swipe

That is why this launch belongs in the broader fintech confession booth SiliconSnark has been cataloging lately. Robinhood's direct-deposit-heavy banking push was not really about vibes or premium branding. It was about owning the account where money lands. Mercury's OCC charter bid was the sponsor-bank era admitting adulthood exists. Circle's institutional stablecoin payments launch was basically crypto dressing up as controlled treasury infrastructure. And XFX trying to clean up the wire-transfer middle came from the same instinct: the most lucrative part of finance is often the shabby handoff everyone else learned to ignore.

LTVX fits that pattern neatly. It is not trying to invent a new way to pay. It is trying to own the liminal state where payment almost happened and then became a support ticket, a lost customer, or an awkward graph in a retention deck. That is deeply enterprise-coded thinking. Very little romance. Considerable margin logic.

I am also reluctantly impressed that the company is not selling merchants on a huge behavior change. That matters. The graveyard is full of payments startups that required consumers to learn a new ritual, download a new wallet, trust a new badge, or perform a small act of faith at the worst possible moment in the funnel. LTVX is trying to fix a problem users already understand viscerally: the thing they wanted to buy failed for a reason nobody can explain in one sentence.

The criticism is simple: this can get creepy fast

Now for the prosecutorial portion of the program.

Any startup that makes money from failed transactions is operating close to a line. The line is trust. Merchants will love the promise of recovered revenue. Consumers will be less enchanted if recovery starts to feel like being pursued by a very upbeat machine with a background in payment orchestration and no respect for social cues. The product only works if the handoff feels legitimate, fast, and obviously connected to the original purchase. Otherwise the same system that looks clever in a growth deck starts to look like collections with nicer CSS.

There is also the issue of platform ambition getting ahead of platform proof. LTVX's site is full of the kinds of claims startups make when they would like to be understood as a full-stack payments power rather than a neat point solution. Sometimes that works. Sometimes it means the company has six adjacent dreams and one fully hardened product. The launch is strongest when it stays narrow: failed card payment, real recovery, merchant revenue saved. Every step beyond that raises the burden of proof.

But even that criticism lands inside a larger compliment. This is one of the more practical fintech launches I have seen lately because the problem is real, the mechanism is legible, and the tone of the product is less "behold, the future of commerce" than "your checkout leaks money and we noticed." That is exactly the kind of insult the market tends to reward.

Verdict: a real enterprise wedge with just enough menace

My verdict is that LTVX.ai looks like a real enterprise hit candidate, not a beautiful overreach. It is targeting a measurable pain point with a pitch that finance teams, growth leads, and payments operators can understand without a translator. The smartest part is not the AI branding. It is the refusal to romanticize the job. This is software for the humiliating moment when revenue was within reach and then wandered into the plumbing.

What feels excessive is the inevitable platform sprawl and the faint sense that every payments company now dreams of becoming an infrastructure state. What feels useful is everything else. If LTVX can actually recover meaningful chunks of legitimate failed volume without turning the post-decline experience into a suspicious side quest, it has found one of the better fintech wedges of the season.

In other words, the company has built a business around the proposition that "payment declined" is not a verdict. It is an invitation to negotiate. Which is a little aggressive, a little funny, and, in the cold fluorescent light of enterprise commerce, kind of neat.