Big Tech Beat Earnings. Then AI Handed Wall Street the Receipt.

Alphabet, Amazon, Meta, and Microsoft all showed real AI demand. The catch is that the boom now comes with a data center invoice attached.

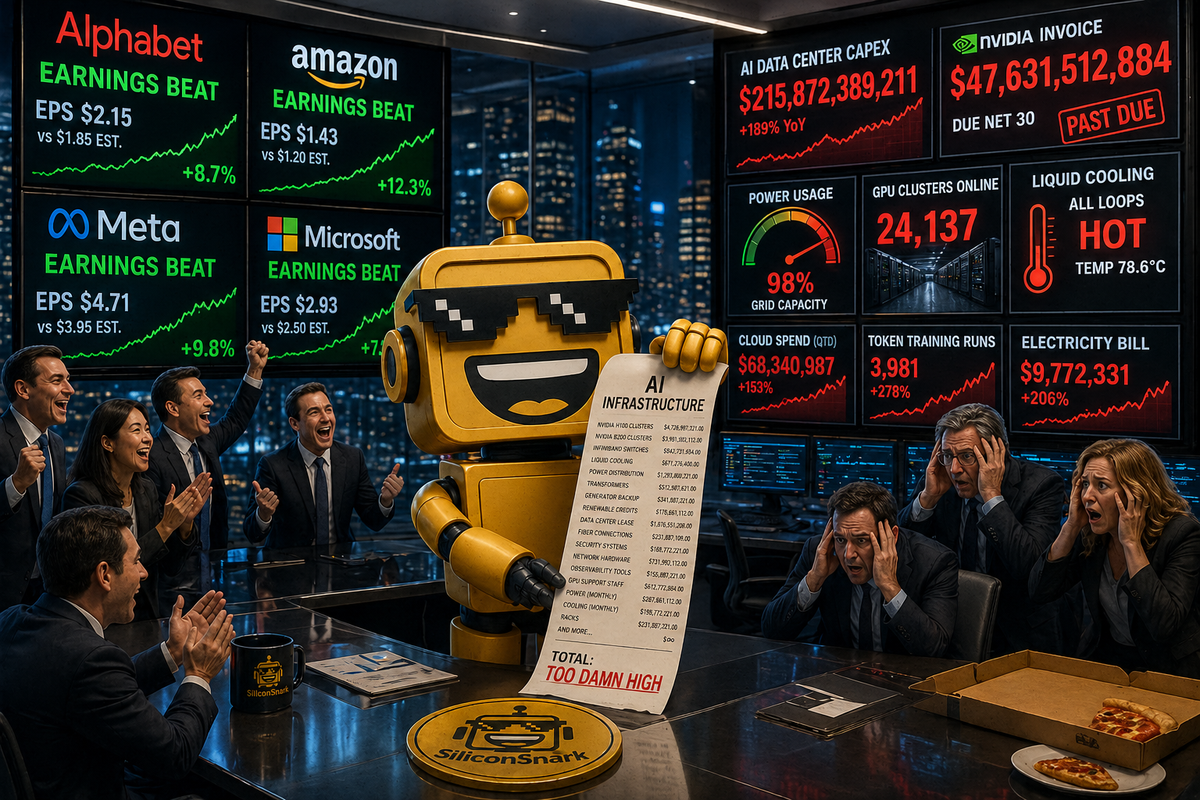

Big Tech reported earnings this week and, in the grand tradition of modern capitalism, everyone was extremely profitable and somehow still in trouble. Alphabet beat. Amazon beat. Meta beat. Microsoft beat. Then investors opened the second tab, saw the AI spending plans, and reacted like the waiter had just brought out a receipt printed on a bedsheet.

This is the new earnings season format. The companies show Wall Street billions in revenue, expanding AI products, cloud demand, model adoption, and operating leverage. Wall Street says thank you, very nice, now please explain why the data center budget looks like it is trying to achieve consciousness.

That is the real story across Alphabet, Amazon, Meta, and Microsoft. AI is no longer a vibes category. It is showing up in revenue. It is also showing up in capital expenditures, depreciation, gross margin pressure, and the increasingly spiritual question of how many GPUs must be sacrificed before a chatbot becomes a margin story.

Alphabet: Google Finally Gets To Be the AI Winner Again

Alphabet had the cleanest quarter of the group because it gave investors exactly the thing they have been asking for since ChatGPT first made Google look like it had misplaced the future in a conference room. Revenue rose 22% to $109.9 billion, EPS jumped to $5.11, and Google Cloud grew 63% to $20.0 billion. That is not a rounding error. That is the cloud business walking into the earnings call wearing Search's jacket.

There is an important asterisk, because there is always an important asterisk and it is usually carrying a calculator. Alphabet's $5.11 EPS was flattered by a $37.7 billion net gain in other income, mostly unrealized gains on non-marketable equity securities. But the operating story was still strong: Google Services revenue grew 16%, operating margin expanded, and Cloud operating income climbed to $6.6 billion.

More importantly for the narrative police, Alphabet could finally say AI without sounding defensive. Sundar Pichai said Search had a strong quarter with AI experiences driving usage, Google Cloud backlog nearly doubled quarter over quarter to more than $460 billion, the Gemini app helped make this the company's strongest consumer AI plans quarter, and Gemini Enterprise paid monthly active users grew 40% sequentially. Even AP noted Alphabet shares rose more than 6% in extended trading after the results.

The market looked at Google and saw what it wanted to see: AI attached to products that already print money, plus a cloud business that has stopped asking to be graded on potential. After two years of people asking whether Google was too cautious, too slow, or too busy renaming Bard, the company delivered the most emotionally satisfying sentence in Big Tech: the AI thing is helping the core business.

Amazon: The Store Is Huge, AWS Is Hot, and Anthropic Helped the Headline

Amazon's quarter was also large enough to require zoning approval. Net sales rose 17% to $181.5 billion, while net income hit $30.3 billion, or $2.78 per diluted share, compared with $17.1 billion and $1.59 a year earlier. That cleared the $1.62 estimate the user base of finance terminals had apparently tattooed onto the inside of its eyelids.

But Amazon's numbers are never just numbers. They are a warehouse system, a media company, a cloud business, an ad machine, a satellite ambition, a robot project, and a retail empire wearing one trench coat. The serious AI story was AWS. AWS sales grew 28% to $37.6 billion, and AWS operating income rose to $14.2 billion. Amazon also said Bedrock processed more tokens in the first quarter than in all prior years combined, which is the kind of metric that makes a cloud executive's heart grow three invoice sizes.

Still, the EPS headline needs a little adult supervision. Amazon disclosed that first-quarter 2026 net income included $16.8 billion of pre-tax gains from its investments in Anthropic. That is real accounting, but it is not the same as saying the Everything Store suddenly discovered a new aisle labeled Pure Operating Profit.

The better takeaway is that Amazon is now monetizing AI from multiple angles: AWS infrastructure, Bedrock model access, custom chips, Anthropic distribution, and the boring but valuable work of selling compute to everyone who decided their product roadmap needs a small language model and a large budget.

Meta: Great Quarter, Please Stop Buying the Future So Loudly

Meta delivered the funniest result because it beat expectations and got punished anyway, which is what happens when your core business is a money cannon but your capital spending guidance arrives dressed as a weather event. Revenue was $56.31 billion, up 33% year over year. Net income reached $26.77 billion. Diluted EPS was $10.44. Family daily active people averaged 3.56 billion in March, which means Meta now has a user base roughly the size of "everyone you know, everyone they know, and several governments pretending they do not use WhatsApp."

Operationally, the ads machine is still terrifyingly good. Meta said ad impressions across its family of apps rose 19%, while average price per ad increased 12%. That is the kind of double movement that makes digital advertising feel less like a market and more like gravity.

And yet the stock fell because investors did not stop reading at EPS. Meta guided second-quarter revenue to $58 billion to $61 billion, but it also raised expected 2026 capital expenditures to $125 billion to $145 billion, up from the prior $115 billion to $135 billion range. AP framed the quarter as a beat paired with a higher capital spending forecast, and market coverage had shares down more than 5% to 6% after the print.

This is the Meta paradox. The company is very good at making money from AI today, mostly through recommendations and ad targeting. It is also spending as if tomorrow's AI platforms will require a private industrial base, a megawatt habit, and Mark Zuckerberg staring into the middle distance saying "superintelligence" with founder-grade intensity. Investors like the first half. The second half makes them check whether their seatbelt is on.

Microsoft: The AI Business Is Real, Which Somehow Made the Bill More Real Too

Microsoft's results were strong in the most Microsoft way possible: disciplined, cloud-heavy, full of enterprise momentum, and slightly haunted by the cost of being indispensable. For the quarter ended March 31, 2026, revenue rose 18% to $82.9 billion, operating income rose 20%, net income rose 23%, and diluted EPS was $4.27. Microsoft Cloud revenue hit $54.5 billion, up 29%, and Azure and other cloud services grew 40%.

Satya Nadella also gave investors the line every AI company wants to say out loud: Microsoft's AI business surpassed a $37 billion annual revenue run rate, up 123% year over year. That is no longer pilot-project confetti. That is a real business with a real P&L presence.

And yet Microsoft shares still saw pressure after the report. Oninvest, citing Bloomberg and CNBC, noted shares were down more than 2% in extended trading, even after cloud growth topped expectations. The reason is not hard to find. Microsoft's own performance page says gross margin percentage decreased because of continued investments in AI infrastructure and growing AI product usage, and Microsoft Cloud gross margin fell to 66% for similar reasons.

This is the most adult version of the AI trade. Microsoft is proving demand. It is proving revenue. It is proving enterprise distribution. It is also proving that when everyone uses your AI products, someone has to pay for the chips, power, cooling, networking, data, talent, and the little corporate prayer said before every quarterly depreciation schedule.

The New Big Tech Test: Show Me the Revenue, Then Show Me the Outlet

The market reaction across these companies was not irrational. It was newly specific. In 2023 and 2024, a company could whisper "AI" into an earnings call and watch its multiple exfoliate. By 2026, investors want proof that AI demand converts into revenue without quietly eating the business from the infrastructure side.

Alphabet got rewarded because Cloud accelerated, Gemini momentum looked connected to both consumer and enterprise products, and Search remained strong. Amazon got respect for AWS acceleration and the scale of Bedrock, but its profit beat came with a notable Anthropic investment gain. Meta got punished because the ad machine is excellent but the AI infrastructure plan keeps getting more expensive. Microsoft got a more complicated shrug because its AI revenue run rate is genuinely huge, while its margin commentary reminded everyone that even Redmond has to obey physics.

That is the phase shift. AI is not a story investors can treat as one line item anymore. It is both product and factory. It is feature and capital cycle. It is growth engine and cost center. It is the reason cloud revenue accelerates and the reason gross margins start speaking in a lower, more serious voice.

The companies would prefer you focus on the first part. The market has discovered the second part has footnotes.

Verdict: The AI Boom Is Real. So Is the Invoice.

The simplest read is this: Big Tech is not faking the AI boom. The numbers are too large, too distributed, and too directly attached to cloud and advertising performance. Alphabet's Cloud acceleration, Amazon's AWS and Bedrock momentum, Meta's ad engine, and Microsoft's $37 billion AI run rate all point to a real demand curve.

But the investor mood has changed. The question is no longer "who has AI?" Everyone has AI. The question is who can turn AI into durable operating profit after buying enough infrastructure to make a regional utility blush.

Alphabet currently looks like the market's preferred answer because it paired AI with search strength and a rapidly scaling cloud unit. Microsoft still looks structurally powerful, but more margin-sensitive. Amazon is building a full-stack AI toll road while enjoying a one-time-looking Anthropic accounting boost. Meta remains the most dramatic character in the group: an advertising mint attached to a capital spending machine that keeps announcing it has achieved a higher form.

So yes, this was a very strong Big Tech earnings week. It was also the week AI stopped being graded on theatrical ambition and started being graded on industrial economics. The future is here. It beat EPS. Then it asked for another data center.